⚡ Quick Answer

Your credit card number isn’t random — it’s a structured code that identifies your card network, your bank, your unique account, and even contains a built-in fraud-detection check digit. Knowing what each part means can help you spot fraud faster, understand how transactions work, and protect your financial life. Every single digit has a job to do.

📋 Quick Summary

Let’s Be Honest — Most of Us Never Think About This

You swipe your card (or tap, or click “pay now”), and the transaction goes through. Done. But that 15- or 16-digit number on the front of your wallet has a whole story packed into it — one that affects your security, how merchants verify your identity, and even whether a fraudulent charge gets stopped before it clears.

Think about it: card fraud cost Americans over $10 billion in 2023 alone. A big chunk of that happens because people don’t understand what makes a card number “real” versus a fake one. The more you know, the harder you are to fool.

So let’s walk through every single part of your credit card number — explained simply, with zero financial jargon.

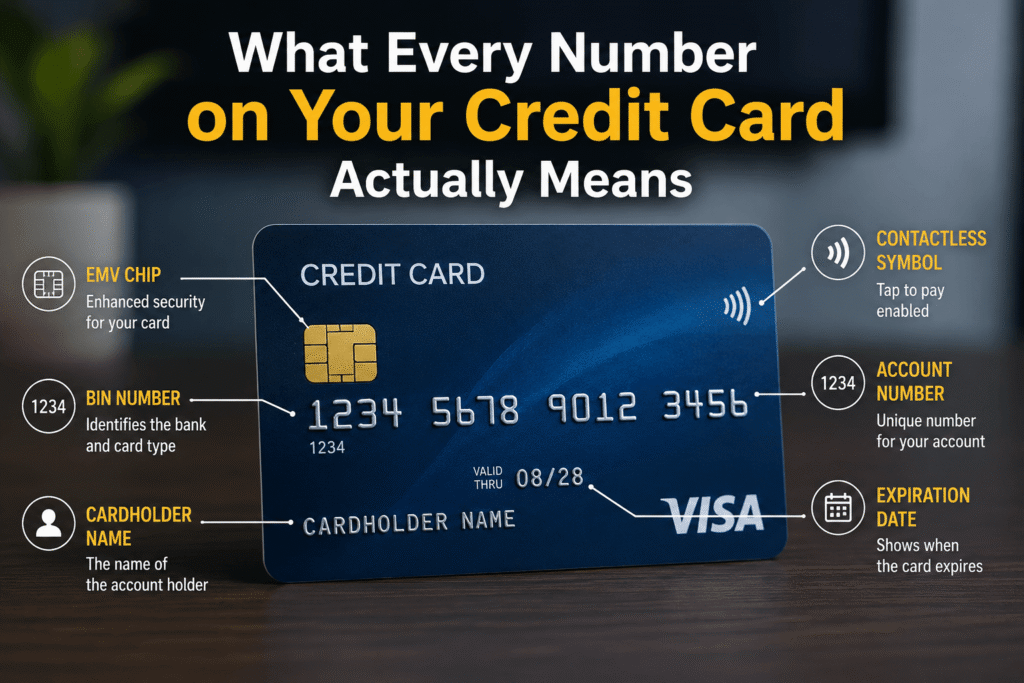

Where Is Your Credit Card Number? (And What Else Is On Your Card?)

Before we break it down digit by digit, let’s get oriented. Your credit card has several pieces of identifying information:

Each one of these has a specific role in processing and securing a transaction. But the main card number? That’s the master key. Let’s break it down.

The Anatomy of a Credit Card Number: Every Digit Explained

Here’s something that might surprise you: your card number is actually governed by an international standard called ISO/IEC 7812. That’s why your Chase Visa works the same way in Minneapolis as it does in Miami — or Madrid.

The First Digit: Major Industry Identifier (MII)

The very first number on your card is called the Major Industry Identifier (MII). It tells the world which industry issued the card. Here’s what each number means:

| First Digit | Industry | Example |

|---|---|---|

| 1, 2 | Airlines | Airline co-branded travel cards |

| 3 | Travel & Entertainment | American Express, Diners Club |

| 4 | Banking & Financial | All Visa cards |

| 5 | Banking & Financial | Mastercard |

| 6 | Merchandising & Banking | Discover, UnionPay |

| 7 | Petroleum | Gas station fleet cards |

| 8 | Healthcare / Telecom | FSA cards, telecoms |

| 9 | Government / Other | Government-issued cards |

💡 Real-life tip: See a charge on your statement from a card starting with “4”? That’s Visa. Starting with “3”? That’s Amex. This can instantly help you figure out which card was used when reviewing suspicious charges.

Digits 1–6: The Issuer Identification Number (IIN) / Bank Identification Number (BIN)

The first six digits of your card number form what’s called the Issuer Identification Number (IIN) — sometimes still referred to as the Bank Identification Number (BIN). This block of numbers tells payment processors:

For example, a Chase Sapphire Preferred card (Visa) will have a different BIN than a Chase Freedom card (also Visa). The BIN is how merchants, processors, and fraud systems instantly recognize who they’re dealing with before the transaction even goes through.

🏦 Why BINs matter for you: When you see those “card declined” messages at checkout, the BIN is often the first place the system checks. Some merchants only accept certain BINs — which is why your corporate card might get declined at a gas pump that only accepts personal cards.

Digits 7–15 (or 7–14 for Amex): Your Unique Account Number

This is the part that’s uniquely yours. After the first six digits (the IIN/BIN), the remaining digits — except for the last one — make up your individual account number.

This sequence is assigned by your card issuer and identifies your specific account within their system. When Chase (or whoever your issuer is) needs to route a transaction to your account specifically, this is the number that does it.

Here’s something worth knowing: if you get a replacement card because yours was lost or stolen, you’ll almost always get a new account number — not just a new card with the same digits. That’s intentional. It cuts off any fraudsters who might have captured your old number.

The Last Digit: The Check Digit (Luhn Algorithm)

The final digit of your credit card number is called the check digit, and it’s one of the most clever — and underappreciated — security features in everyday finance.

It’s calculated using something called the Luhn Algorithm (also called Mod 10), developed by IBM scientist Hans Peter Luhn back in 1954. The algorithm works like this: it performs a series of mathematical operations on the other digits in your card number. The last digit is specifically chosen so that the result of those operations always equals zero (mod 10).

In plain English: if someone types your card number wrong — even by one digit — the check digit will fail the math test. The transaction gets flagged instantly. It’s not foolproof against intentional fraud, but it catches the vast majority of accidental typos and simple fake card numbers.

🔢 Fun fact: You can actually test any credit card number with the Luhn Algorithm yourself. There are free online validators. If the number fails the Luhn check, it’s definitely not a valid card number — regardless of what anyone tells you.

Credit Card Number Formats by Network: Visa vs. Mastercard vs. Amex vs. Discover

Not all card numbers are built the same. Here’s a network-by-network breakdown:

| Network | # of Digits | Starts With | CVV Location |

|---|---|---|---|

| Visa | 16 | 4 | 3 digits, back of card |

| Mastercard | 16 | 51–55 or 2221–2720 | 3 digits, back of card |

| American Express | 15 | 34 or 37 | 4 digits, FRONT of card |

| Discover | 16 | 6011, 622126–622925, 644–649, 65 | 3 digits, back of card |

| UnionPay | 16–19 | 62 | 3 digits, back of card |

| Diners Club | 14 | 300–305, 36, 38 | 3 digits, back of card |

Note: Mastercard expanded its BIN range in 2017 to include 2221–2720. If you have a newer Mastercard starting with “2”, it’s totally normal.

What’s the CVV, CVC, or CID Code? (And Why Is It Separate?)

Your CVV (Card Verification Value) is NOT part of your main card number — but it’s just as important for security. Here’s how each network labels it:

The CVV is calculated using a cryptographic algorithm combining your card number, expiration date, and a secret key only the issuing bank knows. It’s specifically designed so that even if a thief steals your card number (say, from a data breach), they still can’t make a card-not-present online purchase without the CVV.

⚠️ Security rule: No legitimate merchant or bank will EVER ask you to read your CVV out loud on a phone call or enter it on a suspicious website. If someone asks you for it unprompted, that’s a red flag.

Also worth knowing: your CVV is intentionally NOT stored by merchants after a transaction. That’s required by PCI-DSS (Payment Card Industry Data Security Standard). So if a retailer gets hacked, the CVV shouldn’t be in their database — which is one reason it remains an effective security layer. You can learn more about how what is a CVV on our dedicated guide.

Virtual Credit Card Numbers: The 2026 Way to Shop Safer Online

Here’s something SoFi’s article doesn’t cover in depth — and it’s one of the most practical tools you can use right now.

Virtual credit card numbers (VCNs) are temporary, randomly-generated card numbers that link back to your real account without exposing your actual card number. Most major issuers and some third-party apps offer them:

Capital One Eno: Generates virtual numbers right in your browser

Citi Virtual Account Numbers: Lets you set custom spending limits and expiration dates

Privacy.com: Third-party service that works across most banks — lets you create single-merchant or single-use cards

Apple Card: Creates a new virtual card number for every transaction automatically

When should you use a virtual card number? Think free trial subscriptions (where you don’t want to be charged after), sketchy-looking online stores, international websites, or any situation where you’re not 100% sure about a merchant’s security practices.

💳 Affiliate pick: Privacy.com lets you create free virtual cards that work with any bank account. You can set per-merchant spending limits, pause cards instantly, and get notified of every charge — it’s one of the best free fraud-prevention tools most Americans have never heard of.

How Are Credit Card Numbers Generated? (The Part Banks Don’t Advertise)

Your card number didn’t come from a random number generator. It was systematically assigned by your card issuer following ISO/IEC 7812 standards. Here’s the process in plain terms:

This is why the chances of two people accidentally having the same card number are astronomically small — the system is designed to make that nearly impossible.

Tokenization: Why Your Card Number Is Already Hidden at Most Big Retailers

Ever wonder how Apple Pay or Google Pay works? Or why Walmart doesn’t actually store your Visa number in their system?

The answer is tokenization. When you add your card to a digital wallet or pay at a major retailer, your real card number is replaced with a randomly-generated “token” — a substitute number that’s specific to that merchant, device, and sometimes even that transaction.

Here’s what this means for you in practice:

Even if Target or Home Depot gets hacked again, thieves get tokens — which are useless without the matching encryption key

Your actual card number never touches the merchant’s system

Tokens can be instantly revoked without canceling your actual card

This is why cybersecurity experts recommend using Apple Pay, Google Pay, or Samsung Pay wherever possible — especially for in-store purchases. The tokenized transaction is actually MORE secure than swiping your physical card.

🔒 Pro tip: Set up your card in your phone’s digital wallet today if you haven’t already. It takes 2 minutes and meaningfully reduces your fraud exposure — especially at gas stations, which are still the #1 target for card skimmers in the U.S.

How Credit Card Fraud Actually Works — And How Your Number Gets Stolen

Understanding your card number is only half the battle. The other half is knowing how fraudsters get their hands on it. Here are the most common methods in 2026:

1. Card Skimming

Physical devices attached to ATMs, gas pumps, or point-of-sale terminals that read and copy your card’s magnetic stripe data. The skimmer captures your card number and sometimes even a PIN.

Real-world example: In 2023, a skimming ring in Texas compromised over 2,400 cards at gas station pumps over a single weekend before being caught. The cards were physically tapped on the pump — no data breach, no hacking.

2. Phishing

Fake emails, texts, or websites designed to trick you into entering your card number. These look incredibly real — spoofed bank logos, urgent language, and all.

3. Data Breaches

Your card info gets stolen when a merchant, processor, or database you’ve shopped with gets hacked. Between 2020 and 2024, over 1 billion card records were exposed in documented breaches.

4. Card-Not-Present (CNP) Fraud

The most common type of fraud today. A thief uses your stolen card number (and sometimes the CVV) to make online purchases without ever having your physical card.

5. Synthetic Identity Fraud

Criminals combine real card number fragments with fake personal information to create entirely new synthetic identities. This one’s particularly hard to detect and has surged in recent years.

🛡️ Affiliate pick: Identity Guard and Aura both offer real-time dark web monitoring — they’ll alert you within minutes if your card number appears in known data breach databases or shady online marketplaces. Both offer 14-day free trials.

Step-by-Step: How to Protect Your Credit Card Number in 2026

Here’s a practical action plan you can run through today:

What Happens When Your Credit Card Number Gets Stolen? A Real-World Timeline

Here’s what the experience actually looks like — and what you should do at each step:

Your card number gets captured — through a breach, skimmer, or phishing. You have no idea yet.

Fraudsters usually run small “test” transactions first — $1 at a gas station, a small app purchase — to verify the card is active before making larger purchases. This is why transaction alerts are so valuable. That weird $0.99 charge can be the warning shot.

Once they know the card works, purchases escalate. Electronics, gift cards, and luxury goods are favorites because they’re resellable. Time is critical here.

⏱ The faster you report, the better. Under the Fair Credit Billing Act, you have zero liability for unauthorized credit card charges — but you must report them promptly. Debit cards have different (and weaker) protections, which is one more reason financial experts generally recommend credit over debit for everyday purchases.

Credit Card Numbers vs. Debit Card Numbers: What’s Actually Different?

Visually, debit and credit card numbers look identical. Same 16 digits, same format, same CVV on the back. So what’s different?

| Feature | Credit Card | Debit Card |

|---|---|---|

| Fraud liability | $0 (zero liability policy) | Up to $500 if not reported in 2 days |

| Money at risk | Bank’s money (you dispute, then pay) | YOUR money (gone until dispute resolves) |

| Dispute process | Charge reversed immediately while investigated | Funds held until investigation completes |

| PIN usage | Rarely required | Often required |

| Credit score impact | Yes — payment history matters | No direct impact |

| Best for | Online shopping, travel, large purchases | ATM withdrawals, cash needs |

Bottom line: for everyday spending, credit cards offer meaningfully stronger consumer protections than debit cards. This is especially true for online purchases where card-not-present fraud is most common.

What About Routing Numbers? How They Differ from Card Numbers

People sometimes confuse card numbers with routing numbers or account numbers on checks. Quick clarification:

Credit card number: On your credit card. Used for card-based transactions (swiped, tapped, or entered online).

Routing number: A 9-digit number that identifies your bank for ACH transfers, wire transfers, and check processing. It’s printed on the bottom left of your checks.

Bank account number: Identifies your specific checking or savings account. Found on the bottom of your checks, right of the routing number.

These are completely separate systems. Your credit card number has no connection to your routing number. Merchants who ask for both are either doing ACH payments (like a utility company) plus card payments, or something is off — be cautious.

Using Your Card Internationally: What Changes (and What Doesn’t)

Your card number works the same way overseas — the structure doesn’t change. But a few things to know:

Foreign transaction fees: Many cards charge 1–3% on purchases made in foreign currencies. Cards like the Chase Sapphire Preferred, Capital One Venture, and most Amex travel cards waive these.

Dynamic Currency Conversion: When a foreign merchant offers to charge you in U.S. dollars instead of local currency, almost always say no. Their exchange rate is almost always worse than your bank’s rate.

Chip + PIN: Much of Europe and Asia uses chip + PIN systems. American cards mostly use chip + signature. Most modern terminals accept both, but some older European kiosks (train stations, parking meters) may only accept PIN-based cards.

Notify your bank: Technically, most banks no longer require travel notifications, but calling ahead still reduces the chance of your card being flagged for suspicious activity abroad.

Your Credit Card Number and Your Credit Score: What’s the Connection?

Your card number itself doesn’t appear on your credit report — but the account it’s attached to absolutely does. Here’s what impacts your score:

📊 Affiliate pick: Credit Karma and Experian both offer free credit score monitoring with alerts when anything changes. Experian’s free tier even includes FICO score access — not just the VantageScore model — which is what most lenders actually use.

Recommended Tools for Credit Card Security and Monitoring

Here are some practical tools worth considering:

| Tool | Best For | Cost | Standout Feature |

|---|---|---|---|

| Privacy.com | Virtual card numbers | Free / $10/mo Pro | Single-use cards per merchant |

| Aura | Identity & dark web monitoring | ~$12/mo | Real-time breach alerts |

| Identity Guard | Full identity protection | ~$8.99/mo | IBM Watson-powered monitoring |

| Credit Karma | Free credit monitoring | Free | Weekly TransUnion/Equifax updates |

| Experian | FICO score access | Free / $24.99/mo premium | Experian Boost for thin files |

| Apple Pay / Google Pay | Tokenized payments | Free | Eliminates card number exposure in-store |

Frequently Asked Questions

Final Thoughts: Your Card Number Is More Than a Number

Look, most people go their entire lives swiping cards without ever thinking about what those 16 digits actually mean. And honestly? That’s fine, most of the time. The system is designed to work invisibly.

But here’s the thing: the more you understand about how your card number works — what each digit represents, how it protects you, and how fraudsters try to exploit it — the better equipped you are to keep your money safe.

You don’t need to memorize the Luhn Algorithm. You don’t need to know your BIN by heart. But you should know to turn on transaction alerts. You should know what a CVV is and why you don’t hand it out casually. You should know that virtual card numbers exist and that using one for online shopping is one of the easiest free upgrades to your financial security.

Small knowledge, big protection. That’s the whole point.

About This Article: Written by an experienced American personal finance writer for U.S. consumers. This article is for educational purposes only and does not constitute financial or legal advice. Affiliate links may be present — we only recommend tools we’d use ourselves. Last updated: 2026.