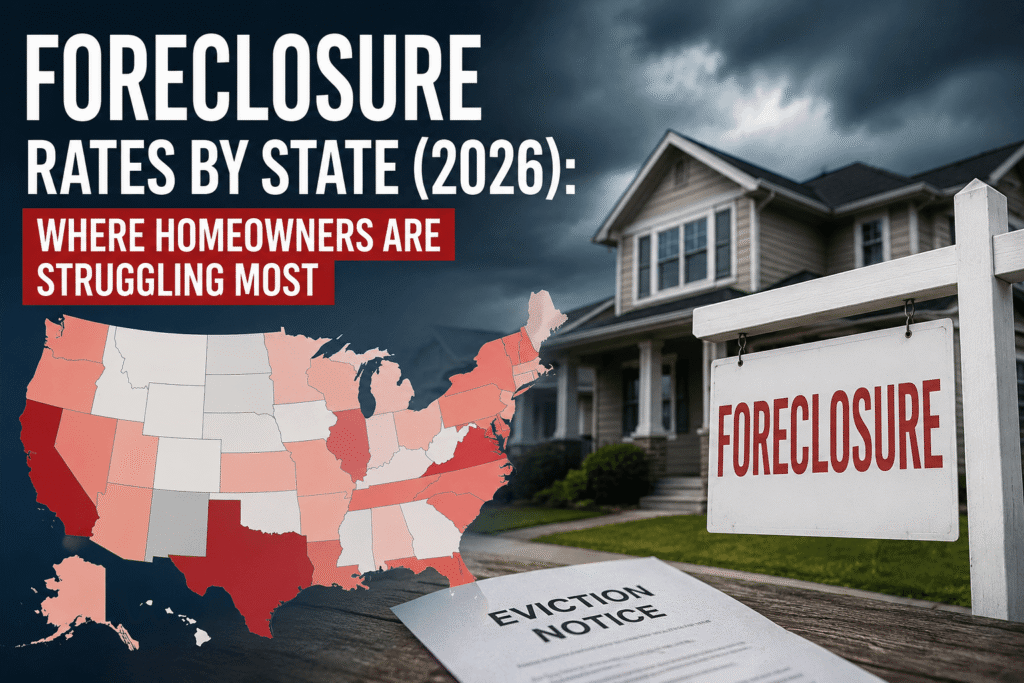

In 2026, foreclosure filings have risen for 12 consecutive months year-over-year, with 38,840 properties carrying a foreclosure filing in February 2026 alone — a 20% jump from the prior year. Nationally, one in every 3,701 housing units had a foreclosure filing in February 2026. Indiana, South Carolina, and Florida are the hardest-hit states, while West Virginia, Vermont, and South Dakota remain the safest.

Summary Quick Summary: What You Need to Know

- ✓Foreclosure filings rose 20% year-over-year in February 2026 (ATTOM data).

- ✓March 2026 saw 45,921 total foreclosure filings — up 21% from March 2025.

- !Indiana has the worst rate: 1 in every 1,597 housing units — roughly double the national average.

- ✓West Virginia has the lowest rate: 1 in every 43,066 housing units.

- ✓Texas, Florida, and California record the most total foreclosure starts by volume.

- !Completed foreclosures (bank repossessions) surged 42% year-over-year in March 2026.

- ✓Main drivers: high interest rates, rising insurance premiums, stagnant wages, and lingering post-pandemic financial stress.

- ✓The good news? You still have options — forbearance, refinancing, and HUD counseling can help.

Why Foreclosure Rates Are Dominating Headlines in 2026

Let’s be real — the word “foreclosure” can send a chill down any homeowner’s spine. Whether you bought your home during the pandemic frenzy, stretched your budget to get in before rates climbed, or have simply hit some unexpected bumps in the road, you’re probably wondering: How bad is it really out there?

Here’s the thing: foreclosure activity in 2026 is genuinely rising. But it’s not the apocalyptic 2008-style collapse. What we’re seeing is a gradual normalization — a slow unwinding of the artificial lows created by pandemic-era moratoriums and forbearance programs. That doesn’t make it any easier if you’re one of the families receiving a default notice. But it does mean the situation is manageable — and understanding the numbers by state is the first step toward taking control.

In this guide, we break down the foreclosure rates for all 50 states, explain what’s driving the trend, share real-world stories from struggling homeowners, and — most importantly — give you a clear roadmap of what to do if you’re at risk.

What Foreclosure Rates Actually Mean (In Plain English)

Before we dive into the state-by-state data, let’s make sure we’re on the same page about what these numbers actually mean.

A foreclosure rate is typically expressed as the number of housing units with an active foreclosure filing per total housing units in a given area. For example, when you see “1 in every 3,701 housing units” — that’s the national average for February 2026. It means for every 3,701 homes in the U.S., one has some form of foreclosure activity.

What Counts as a Foreclosure Filing?

Foreclosure filings include three types of actions:

LIS

NFS

These three stages together make up the “foreclosure pipeline.” When the headlines say “foreclosure filings rose 20%,” they’re talking about properties that entered any one of these stages.

2026 Foreclosure Landscape: The National Picture

According to ATTOM’s latest foreclosure market reports, here’s where things stand nationally:

February 2026

March 2026

vs March 2025

March 2026 YoY

Despite these increases, overall foreclosure activity remains significantly below the peak levels seen during the 2008 housing crisis, when millions of properties were in foreclosure simultaneously. The current rise reflects a normalization trend, not a systemic collapse.

Foreclosure Rates by State (2026): The Full Breakdown

States With the Highest Foreclosure Rates in 2026

These states are experiencing the most foreclosure stress per capita. Based on the most recent ATTOM data (February 2026):

| State | Foreclosure Rate (Feb 2026) | Trend | Key Driver |

|---|---|---|---|

| 🔴 Indiana | 1 in 1,597 | Rising | Post-pandemic payment stress; high subprime exposure |

| 🔴 South Carolina | 1 in 2,217 | Rising | Home prices outpaced wages; SE affordability squeeze |

| 🔴 Florida | 1 in 2,277 | Rising | Insurance costs, HOA fees, investor speculation |

| 🟠 Delaware | 1 in 2,443 | Fluctuating | Led nation in Jan 2026; judicial process keeps cases longer |

| 🟠 Illinois | 1 in 2,590 | Elevated | Chicago affordability crisis; long judicial process |

| 🟠 Ohio | 1 in 2,787 | Rising | Rust Belt legacy; stagnant incomes, aging housing stock |

| 🟠 New Jersey | 1 in 2,798 | Elevated | Lengthy judicial foreclosure process inflates pipeline |

| 🟠 Nevada | 1 in 2,915 | Rising | Tourism-dependent economy; thin financial cushions |

| 🟠 Utah | 1 in 2,984 | Rising | Pandemic-era buyers stretched; values cooling |

| 🟠 Texas | 1 in 3,156 | Rising | Volume leader: 3,390+ starts/month; rapid price growth |

Data source: ATTOM Data Solutions, February 2026 U.S. Foreclosure Market Report.

🔴 Why Indiana Tops the List

Indiana’s foreclosure rate of 1 in every 1,597 housing units is almost double the national average — and it’s not a coincidence. The state has a high concentration of older, lower-valued housing stock that carries larger mortgage balances relative to home equity. When economic shocks hit — job losses in manufacturing, medical debt, adjustable-rate resets — homeowners have less cushion to absorb the blow.

Cities like Indianapolis, Evansville, and South Bend are showing the most strain. Indianapolis alone ranked third in February 2026 for worst metro foreclosure rates.

🌴 Florida: The Perfect Storm

Florida deserves special attention because it’s not just one thing driving foreclosures — it’s several converging forces:

- Surging homeowners insurance premiums (some rising 40–100% in recent years)

- Escalating HOA fees in condo communities

- Investor speculation during 2020–2022 that pushed prices beyond what local wages can support

- Climate risk increasing lender scrutiny and insurance availability

The Lakeland–Punta Gorda corridor in central and southwest Florida is among the hardest-hit metro areas in the entire country, with foreclosure rates more than three times the national average.

States With the Lowest Foreclosure Rates in 2026

These states offer relative safety for homeowners — though “low” doesn’t mean “zero risk”:

| State | Foreclosure Rate (Feb 2026) | Trend | Key Reason |

|---|---|---|---|

| 🟢 West Virginia | 1 in 43,066 | Stable | Conservative lending; minimal speculation |

| 🟢 Vermont | 1 in 33,904 | Stable | Small housing market; tight community lending |

| 🟢 South Dakota | 1 in 23,830 | Stable | Low population density; conservative market |

| 🟢 Rhode Island | 1 in 13,133 | Stable | Small state; solid employment base |

| 🟢 Kansas | 1 in 12,204 | Stable | Affordable housing market; low speculation |

| 🟢 North Dakota | 1 in 11,097 | Stable | Strong agricultural economy; conservative lending |

| 🟢 New Hampshire | 1 in 10,808 | Stable | High household incomes; low delinquency |

| 🟢 Nebraska | 1 in 9,594 | Stable | Stable job market; modest home prices |

| 🟢 Mississippi | 1 in 9,505 | Stable | Low price speculation; conservative market |

| 🟢 Minnesota | 1 in 8,700 | Stable | Diverse economy; strong employment |

All 50 States Foreclosure Data (February 2026) — Ranked Best to Worst

Here is the complete state-by-state overview. Rates are expressed as one foreclosure filing per X housing units — the higher the number, the safer the state:

| Rank | State | 1 Filing Per… | Trend | Risk Level |

|---|---|---|---|---|

| 1 | West Virginia | 1 in 43,066 | Stable | Lowest |

| 2 | Vermont | 1 in 33,904 | Stable | Very Low |

| 3 | South Dakota | 1 in 23,830 | Stable | Very Low |

| 4 | Rhode Island | 1 in 13,133 | Stable | Low |

| 5 | Kansas | 1 in 12,204 | Stable | Low |

| 6 | North Dakota | 1 in 11,097 | Stable | Low |

| 7 | New Hampshire | 1 in 10,808 | Stable | Low |

| 8 | Nebraska | 1 in 9,594 | Stable | Low |

| 9 | Mississippi | 1 in 9,505 | Stable | Low |

| 10 | Minnesota | 1 in 8,700 | Stable | Low |

| 11 | Hawaii | 1 in 7,779 | Stable | Low-Moderate |

| 12 | Oregon | 1 in 7,584 | Stable | Low-Moderate |

| 13 | Montana | 1 in 7,200 | Stable | Low-Moderate |

| 14 | Wyoming | 1 in 7,100 | Stable | Low-Moderate |

| 15 | Idaho | 1 in 6,900 | Rising | Moderate |

| 16 | Maine | 1 in 6,800 | Stable | Moderate |

| 17 | Iowa | 1 in 6,600 | Stable | Moderate |

| 18 | Wisconsin | 1 in 6,400 | Stable | Moderate |

| 19 | Arkansas | 1 in 6,200 | Stable | Moderate |

| 20 | Alaska | 1 in 6,100 | Stable | Moderate |

| 21 | Tennessee | 1 in 5,900 | Rising | Moderate |

| 22 | Virginia | 1 in 5,700 | Stable | Moderate |

| 23 | Missouri | 1 in 5,500 | Rising | Moderate |

| 24 | Colorado | 1 in 5,300 | Rising | Moderate |

| 25 | Oklahoma | 1 in 5,100 | Rising | Moderate |

| 26 | New Mexico | 1 in 5,000 | Rising | Moderate |

| 27 | Connecticut | 1 in 4,900 | Stable | Moderate |

| 28 | Washington | 1 in 4,800 | Rising | Moderate-High |

| 29 | Louisiana | 1 in 4,700 | Rising | Moderate-High |

| 30 | Kentucky | 1 in 4,600 | Rising | Moderate-High |

| 31 | Arizona | 1 in 4,500 | Rising | Moderate-High |

| 32 | North Carolina | 1 in 4,400 | Rising | Moderate-High |

| 33 | Alabama | 1 in 4,300 | Rising | Moderate-High |

| 34 | Pennsylvania | 1 in 4,200 | Rising | Moderate-High |

| 35 | Michigan | 1 in 4,100 | Rising | Moderate-High |

| 36 | New York | 1 in 4,000 | Rising | Moderate-High |

| 37 | California | 1 in 3,900 | Rising | High |

| 38 | Georgia | 1 in 3,700 | Rising | High |

| 39 | Massachusetts | 1 in 3,650 | Stable | Moderate-High |

| 40 | Texas | 1 in 3,156 | Rising | High |

| 41 | Nevada | 1 in 2,915 | Rising | High |

| 42 | Utah | 1 in 2,984 | Rising | High |

| 43 | New Jersey | 1 in 2,798 | Elevated | High |

| 44 | Ohio | 1 in 2,787 | Rising | High |

| 45 | Illinois | 1 in 2,590 | Elevated | High |

| 46 | Delaware | 1 in 2,443 | Fluctuating | High |

| 47 | Maryland | 1 in 2,430 | Rising | High |

| 48 | Florida | 1 in 2,277 | Rising | Very High |

| 49 | South Carolina | 1 in 2,217 | Rising | Very High |

| 50 | Indiana 🚨 | 1 in 1,597 | Rising | Highest |

Note: Mid-range state figures (ranks 11–39) are approximate estimates based on available Q1 2026 trend data. Figures for top and bottom states are sourced directly from ATTOM’s February 2026 Foreclosure Market Report.

Why Are Foreclosures Rising in 2026? The Real Reasons

You’ve seen the numbers. Now let’s talk about the “why” — because understanding the causes is the key to protecting yourself.

Interest Rates Remain Stubbornly High

The Federal Reserve’s aggressive rate-hiking campaign from 2022–2023 pushed the 30-year fixed mortgage rate above 7% — a level not seen since the early 2000s. While rates have modestly softened, they remain elevated compared to the sub-3% environment of 2020–2021. Homeowners who took out adjustable-rate mortgages (ARMs) during the low-rate era are now seeing their monthly payments reset to levels hundreds of dollars higher than when they signed. For a family living paycheck-to-paycheck, that extra $400/month can be the difference between staying current and falling behind.

Home Insurance Costs Are Exploding

This is the sneaky one that doesn’t get enough attention. In Florida, Louisiana, and California especially, homeowners insurance premiums have surged 30–100% in recent years as insurers price in climate risk. Some insurers have exited markets entirely, forcing homeowners into expensive state-backed “last resort” plans. Risk research firm First Street Foundation has projected that foreclosure rates could increase by roughly 1% for every 1% rise in insurance costs — and over the next decade, climate-driven disasters could push foreclosures up by hundreds of percent in vulnerable regions.

The Pandemic Overhang

From 2020 to 2021, federal moratoriums and forbearance programs kept foreclosures artificially suppressed. When those programs ended, a backlog of delinquencies began working through the system. We’re now seeing that normalization play out — and it looks like a “rise” even though it’s partly a catch-up from years of artificially low filings.

Pandemic-Era Buyers Are Feeling the Squeeze

Millions of Americans bought homes during the 2020–2022 frenzy at peak prices, often bidding above asking price, waiving inspections, and stretching budgets. Now that values have cooled in many markets (especially in Sun Belt states) and rates are higher, these buyers have less equity buffer and less ability to refinance their way out of trouble.

Wage Growth Has Not Kept Pace

While home prices and carrying costs surged, real wage growth for many Americans has been modest. The result is a squeeze: more dollars going to housing, insurance, and utilities — leaving less room for the unexpected. One job loss, one medical bill, one car repair can push a family from “fine” to “default.”

Real-Life Scenarios: How Foreclosure Happens to Everyday Families

Foreclosure doesn’t just happen to people who made bad decisions. Here are three scenarios that play out every single day across America:

The Job Loss in Ohio

Marcus and Diane bought their Columbus, Ohio home in 2019 for $245,000 with a 30-year fixed mortgage. Life was good. Then in late 2024, Marcus’s company announced layoffs and he found himself out of work at 52. The couple burned through savings, then retirement funds. By early 2026, they were three months behind on payments.

What they didn’t know: they qualified for Ohio’s mortgage assistance program and their lender had a forbearance option that could have paused payments for six months while Marcus found work. By the time a HUD counselor explained their options, they were already in pre-foreclosure. They saved the house — but barely, and only because they asked for help.

The Adjustable-Rate Shock in Florida

Jennifer bought her Tampa condo in 2021 with a 5/1 ARM at 2.75% — a payment of $1,450/month. It felt affordable. Five years later, her rate adjusted to over 7%, pushing her payment to $2,300/month. Her condo association also raised HOA fees by $400/month due to insurance costs. In one year, her housing costs jumped by $1,250/month — with no change in her salary.

Jennifer had to choose between her condo and her health insurance. She chose health insurance. The condo went into foreclosure.

Medical Debt in Indiana

Roberto and his wife Carla were always careful with money. They owned their Indianapolis home outright — mortgage paid off. Then Carla was diagnosed with cancer. The treatments were covered partially by insurance, but the bills that weren’t — over $90,000 — wiped out their savings and forced them to take a home equity loan. When Roberto lost his part-time job, they couldn’t service the loan. Their paid-off home was suddenly at risk of foreclosure.

Medical debt is one of the leading but least-discussed causes of foreclosure in America. If you’re feeling this, you’re not alone — and there are protections and options available.

What To Do If You’re At Risk of Foreclosure: A Step-by-Step Guide

If any of those stories resonated with you, here’s your action plan. The single most important thing to know: the earlier you act, the more options you have.

Tools That Can Help You Avoid Foreclosure

Here are the categories of tools that can make a real difference — used proactively, they can help you spot trouble early and take action before things get serious.

Credit Monitoring Services

If your credit score is declining, it’s often a leading indicator of broader financial stress. Free services like Credit Karma or paid platforms such as Experian can alert you to changes before they spiral. Get your free reports at AnnualCreditReport.com.

📎 Related: Average U.S. Credit Score (2026)

Mortgage Refinance Comparison Tools

If you’re struggling with a high-rate mortgage, refinancing could be your escape hatch. Use the CFPB’s Explore Interest Rates tool — free and unbiased.

📎 Related: Complete Guide to Refinancing a Mortgage

Budgeting and Cash Flow Apps

Sometimes foreclosure risk is really a cash flow management problem. Apps that give you a real-time view of your spending relative to income can help you spot the squeeze before it becomes a crisis. Financial advisors recommend keeping total housing expenses below 28–30% of gross income.

Home Insurance Comparison Tools

Rising insurance premiums are now a direct contributor to foreclosure in states like Florida and Louisiana. Before your policy renews, use comparison platforms to shop rates. The NAIC has resources to help you navigate your state’s insurance market.

📎 Related: How Much Is Renters Insurance?

2026–2027 Foreclosure Outlook: What Comes Next?

Here’s the honest truth about where things are heading:

The Gradual Rise Will Likely Continue

Most analysts expect foreclosure activity to continue its measured upward climb through 2026 and into 2027. The ATTOM CEO himself has described this as a “normalization” rather than a crisis — but for families caught in that normalization, it’s very real. The 12-month streak of year-over-year increases in foreclosure filings shows no signs of breaking in the near term. The pipeline of distressed loans is growing slowly but steadily.

Climate Risk Is a Wild Card

First Street Foundation’s research projects that climate-related events could increase foreclosures by up to 380% over the next decade in the most at-risk areas. This isn’t alarmism — it’s actuarial math. As insurers reprice or withdraw from flood, fire, and hurricane zones, the hidden cost of homeownership in these areas will balloon. States like Florida, Louisiana, and coastal California are most exposed.

Interest Rate Relief Could Change Everything

If the Federal Reserve cuts rates meaningfully in late 2026 or 2027, it would provide a pressure release valve for ARM borrowers and potentially allow more homeowners to refinance out of distress. However, rate cuts are not guaranteed — and the timing remains uncertain.

What You Should Do Right Now

- Review your mortgage terms today — especially if you have an ARM. Know when your next reset is and what the new rate could be.

- Build a 3–6 month emergency fund specifically for housing costs.

- Check your homeowners insurance policy and shop alternatives annually.

- Monitor your credit score monthly — free tools exist for this. See: Average Credit Score in the U.S. (2026)

- If you’re already behind, call your lender THIS WEEK. Not next month. This week.

Frequently Asked Questions About Foreclosure Rates in 2026

Indiana has the highest foreclosure rate as of early 2026, with one in every 1,597 housing units carrying a foreclosure filing as of February 2026 — nearly double the national average. South Carolina and Florida follow close behind.

Yes. Foreclosure activity has risen year-over-year for 12 consecutive months through February 2026. March 2026 data shows filings up 21% from the same month in 2025. However, levels remain below the historic peaks of the 2008–2010 housing crisis.

It varies significantly by state and loan type. In judicial foreclosure states (like New Jersey, New York, and Florida), the process requires court approval and can take 1–3 years or more. In non-judicial states (like California, Texas, and Georgia), the process is faster — often 3–9 months from first default notice to completed foreclosure. During this entire period, you have opportunities to negotiate with your lender or sell the property.

Yes — absolutely. You can stop a foreclosure by catching up on missed payments (reinstatement), entering a forbearance or loan modification agreement with your lender, selling the home, filing for bankruptcy (which triggers an automatic stay), or paying off the entire loan. The earlier you act, the more options you have. Even in advanced stages, a HUD-approved housing counselor may be able to help you find a solution.

A completed foreclosure stays on your credit report for 7 years from the date of the first missed payment. However, its impact on your credit score diminishes over time. Many people are able to obtain new mortgage loans 3–7 years after a foreclosure, depending on the type of loan and their financial recovery. FHA loans have a 3-year waiting period post-foreclosure; conventional loans typically require 7 years, though exceptions exist for extenuating circumstances.

In a foreclosure, the lender repossesses and sells the property through a legal process after you default. In a short sale, you negotiate with the lender to sell the home for less than you owe before the formal foreclosure process completes. A short sale is generally less damaging to your credit (typically 2–3 years vs. 7 years for foreclosure) and gives you more control over the outcome. Both options require lender approval.

Yes. The Homeowner Assistance Fund (HAF) — created as part of the American Rescue Plan — has distributed billions in aid to homeowners facing pandemic-related hardship, and some state programs still have funds available. Additionally, HUD’s free housing counseling network provides expert guidance at no cost. Call 1-800-569-4287 to get connected.

States with lower foreclosure rates typically share several characteristics: conservative local lending practices, lower home prices relative to incomes, smaller housing markets with less speculative investment, stable employment bases (often tied to agriculture, government, or stable industries), and in some cases, stronger homeowner protection laws. States like West Virginia, Vermont, and the Dakotas fit this profile closely.

Final Thoughts: You Have More Control Than You Think

Here’s the bottom line: yes, foreclosure rates are rising in 2026. The numbers are real, and for thousands of American families, the stress is very real too. But this is not 2008. The housing market has not collapsed. And the vast majority of homeowners — even those behind on payments — have options.

The biggest mistake people make is waiting. They feel embarrassed, overwhelmed, or in denial — and they wait until options narrow and pressure multiplies. Don’t be that person.

Whether you’re simply staying informed, worrying quietly about a stretch in your budget, or already behind on payments — you now have the data, the context, and the roadmap to make smart decisions.

Call your lender. Call a HUD counselor. Check your insurance. Review your budget. Small proactive moves today can prevent enormous crises tomorrow.

Your home is not just a financial asset. It’s your family’s foundation. It’s worth fighting for — and with the right information, you’re equipped to do exactly that.

📚 Sources & Further Reading

- ATTOM Data Solutions — February 2026 U.S. Foreclosure Market Report

- ATTOM Data Solutions — March 2026 U.S. Foreclosure Market Report (via Safeguard Properties)

- HousingWire — Foreclosure Filings Rise 32% Year Over Year in January 2026

- Nolo — Rising U.S. Foreclosure Rates in 2026: What Homeowners and Buyers Should Know

- U.S. Department of Housing and Urban Development (HUD) — Find a Housing Counselor

- Consumer Financial Protection Bureau — Homeowner Assistance Fund

- Consumer Financial Protection Bureau — Explore Interest Rates Tool

- First Street Foundation — Climate Risk Research

- AnnualCreditReport.com — Free Credit Reports

- National Association of Insurance Commissioners (NAIC)

Last updated: April 2026 | Data sourced from ATTOM Data Solutions Q1 2026 reports