High-yield savings accounts are far superior to traditional savings accounts for building wealth — and it’s not even close. With APYs of 4% to 5%+ compared to the 0.01% to 0.50% you’ll find at most big banks, a high-yield account can earn you hundreds or even thousands of dollars more per year on the same balance. If you’re parking money in a traditional savings account right now, you’re leaving real money on the table every single day.

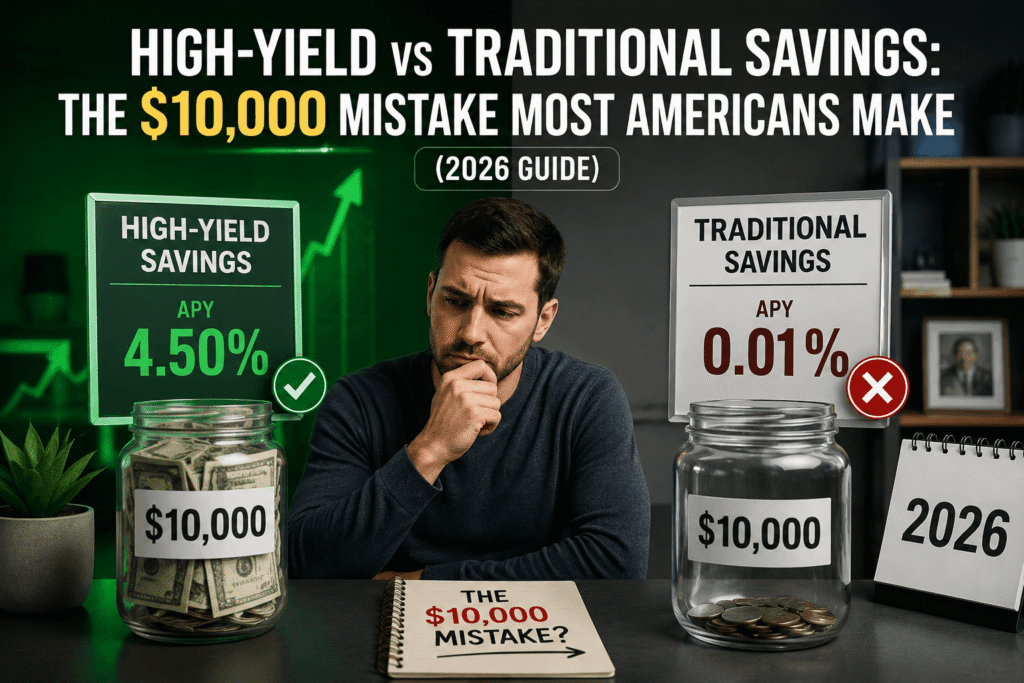

- ✓ High-yield savings accounts (HYSAs) currently offer APYs of 4.00%–5.25%, while traditional accounts earn as little as 0.01%.

- ✓ On a $10,000 balance, a HYSA earns roughly $475/year vs. just $1 in a traditional account — a difference of $474.

- ✓ Both account types are FDIC-insured up to $250,000, so safety is equal.

- ✓ HYSAs are mostly online-only, but that’s a feature, not a flaw — they’re accessible 24/7 and have fewer fees.

- ✓ Switching to a high-yield account takes about 10–15 minutes and can be done entirely online.

- ✓ If you’re saving for an emergency fund, a vacation, a car, or a down payment — a HYSA is the smarter choice.

- ✓ The only real edge traditional accounts have is in-person branch access — and for most people, that’s not worth hundreds of dollars a year.

What Is a High-Yield Savings Account?

A high-yield savings account is exactly what it sounds like — a savings account that pays you a significantly higher interest rate than a standard bank account. These accounts are typically offered by online banks and fintech companies like Marcus by Goldman Sachs, Ally Bank, SoFi, and Marcus. Because they don’t have the overhead of maintaining physical branches, they pass those savings on to you in the form of better interest rates.

In 2026, the best high-yield savings accounts are offering APYs (Annual Percentage Yields) in the range of 4.00% to 5.25%. That might not sound revolutionary, but the math tells a very different story — especially over time.

Here’s what you should know about HYSAs:

Think of a high-yield savings account as your regular savings account’s smarter, higher-earning cousin. Same protection, same accessibility — just way better returns.

What Is a Traditional Savings Account?

A traditional savings account is the kind of account most of us were taught to open when we got our first job — the one your brick-and-mortar bank offered alongside your checking account. It’s a safe, federally insured place to store money you don’t need right away.

The catch? The interest rates are almost embarrassingly low.

As of 2026, the national average APY on a traditional savings account sits at around 0.41% — but the big banks like Chase, Bank of America, and Wells Fargo often pay far less, some as low as 0.01%. That means on a $10,000 balance, you might earn exactly… $1. Per year.

Traditional savings accounts do have some advantages:

- • In-person branch access if you prefer face-to-face banking

- • Often bundled with checking accounts for easy transfers

- • Familiar interfaces and long-standing brand trust

- • Some offer ATM card access

But let’s be honest — those perks aren’t worth leaving hundreds or thousands of dollars in potential earnings behind. The low rates aren’t a glitch in the system. For big banks, it’s the business model. They profit from the difference between what they earn on your money and the paltry amount they pay you.

“Letting your money sit in a traditional savings account is like doing all the right things — working hard, setting money aside — but then leaving your wallet on the counter instead of putting it in your pocket.”

High-Yield vs Traditional Savings: The Real Difference

So why are so many people still using traditional savings accounts? Mostly inertia — they opened one at their bank years ago and never thought twice about it. But once you see the numbers side by side, it’s hard to go back.

Let’s break this down category by category.

Interest Rates

This is the big one. The gap between high-yield and traditional savings rates in 2026 is massive:

That’s a difference of roughly 40x to 500x more interest. On a $5,000 balance, you’d earn $5 per year in a traditional account versus $237.50 in a high-yield account. On $20,000, the gap is $20 vs. $950. The math doesn’t lie.

Accessibility

Traditional accounts win here — but barely. They offer branch access if you need to speak to someone in person or deposit cash. High-yield accounts are almost exclusively online, which can feel limiting.

That said, most people handle all their banking digitally already. If you have a separate checking account at your regular bank (which most people do), you won’t miss the branch access for your savings at all.

Safety

Both account types are FDIC-insured up to $250,000 per depositor, per institution. So this is a tie — your money is equally safe at an online bank as it is at a major national bank. The FDIC doesn’t care where your bank has its offices.

A common fear is: “Is my online bank trustworthy?” The answer is yes — as long as you verify it’s FDIC-insured. You can confirm at FDIC.gov in under 30 seconds.

Fees

Traditional savings accounts at big banks often charge monthly maintenance fees ranging from $5 to $15 per month unless you maintain a minimum balance. That’s up to $180 per year just to keep your account open.

Most high-yield savings accounts? Zero monthly fees. No minimum balance requirements either. That’s another hidden way HYSAs come out ahead — they’re not quietly draining your account while you sleep.

Convenience

This one’s closer than you’d think. Traditional banks have mobile apps and online portals too, so day-to-day convenience is fairly similar. The main edge traditional banks have is the physical branch network for things like depositing cash or getting certified checks.

High-yield savings accounts, however, often have cleaner mobile apps, better savings tools, and features like automated round-ups and goal-setting that make it easier to stay on track with your financial goals.

Side-by-Side Comparison Table

| Feature | 🏆 High-Yield Savings | Traditional Savings |

|---|---|---|

| Interest Rate (APY) | 4.00% – 5.25% (2026 avg) | 0.01% – 0.50% |

| Accessibility | Online/mobile (24/7) | Branch + online |

| FDIC Insured | ✅ Yes (up to $250,000) | ✅ Yes (up to $250,000) |

| Monthly Fees | None (most online banks) | Often $5–$15/month |

| Minimum Balance | $0 – $1 (most providers) | $100 – $500 (typical) |

| Best For | Growing emergency fund, saving goals | Everyday cash access, branch lovers |

| Ease of Switching | Takes 10–15 minutes online | Already set up |

Wealth Growth Breakdown: The Numbers That Will Make You Switch

Let’s get real with some actual numbers. Here’s how $5,000 grows over time depending on which type of account you use. We’re assuming a traditional savings rate of 0.10% APY and a high-yield rate of 4.75% APY — both realistic 2026 figures.

| Timeframe | $5,000 Traditional (0.10%) | $5,000 High-Yield (4.75%) | Difference |

|---|---|---|---|

| 1 Year | $5,005.00 | $5,237.50 | +$232.50 |

| 2 Years | $5,010.01 | $5,486.14 | +$476.13 |

| 3 Years | $5,015.02 | $5,746.87 | +$731.85 |

| 5 Years | $5,025.06 | $6,297.63 | +$1,272.57 |

| 10 Years | $5,050.25 | $7,920.20 | +$2,869.95 |

Let that sink in. Over 10 years, the person with a high-yield savings account ends up with $2,869 more — from the exact same initial deposit. That’s not investing. That’s not taking risks. That’s simply choosing the right type of savings account.

Now scale that to $10,000, $25,000, or your full emergency fund. The numbers get even more dramatic. This is why personal finance experts consistently recommend high-yield savings accounts as the baseline for anyone who isn’t actively investing their savings.

“The $10,000 mistake isn’t a single bad decision. It’s years of earning almost nothing on your savings when you could have been quietly building wealth — automatically.”

Real-Life Examples: What This Looks Like in Practice

Sarah is a 34-year-old nurse in Ohio with $12,000 sitting in her Chase savings account earning 0.01% APY. She heard about high-yield savings accounts from a podcast and figured she’d look into it.

In 15 minutes, she opened an account with an online bank offering 4.85% APY. She transferred her $12,000 and set up automatic transfers of $300 per month from her checking account.

Here’s how things changed:

- ✓ Year 1: Earned $582 in interest (vs. $1.20 at Chase)

- ✓ Year 2: Earned $610 in interest, now has over $20,000 saved including contributions

- ✓ Total interest earned in 2 years: ~$1,192 extra

Sarah didn’t change her spending habits, didn’t invest in anything risky, and didn’t give up access to her money. She just moved it somewhere smarter.

Mike is a 41-year-old contractor in Texas. He’s been with the same regional bank for 15 years and keeps his $18,000 emergency fund in their savings account at 0.05% APY. It feels safe and familiar, so he’s never thought much about it.

Over 5 years, Mike earns about $45 in interest on his $18,000. In that same period, if he’d moved to a high-yield account at 4.75%, he would have earned roughly $4,680 in interest.

Mike left $4,635 on the table — not because of bad luck, but because of inertia.

This isn’t a criticism of Mike. It’s a reality check for all of us. The system rewards people who ask questions, and it quietly benefits from those who don’t.

How to Switch to a High-Yield Savings Account (Step-by-Step)

Ready to make the switch? Good news — it’s easier than ordering a pizza. Here’s exactly what to do:

Start by looking at currently available rates. Reputable comparison tools like NerdWallet, Bankrate, and DepositAccounts aggregate live APYs across dozens of providers. Look for accounts with no monthly fees, no minimum balance, and strong user reviews. In 2026, top picks often include online banks and fintech platforms that regularly update their rates to stay competitive.

Before opening any account, confirm the bank is FDIC-insured at FDIC.gov. This takes 30 seconds and ensures your deposits up to $250,000 are federally protected — the same protection you get at any major bank.

Most high-yield savings accounts can be opened in 10–15 minutes entirely online. You’ll typically need your Social Security number, a government-issued ID, and your existing bank’s routing and account number for the initial deposit. No branch visit required.

Transfer your savings from your traditional account to your new high-yield account. This usually takes 1–3 business days. Keep a small buffer in your old account if you have any automatic payments tied to it.

This is where the magic really happens. Set up an automatic transfer from your checking account to your new high-yield savings account each payday. Even $50 per week compounds meaningfully at 4%+ APY. Many apps let you round up purchases and sweep the difference automatically.

You don’t have to close your traditional savings account right away. Many people keep a small balance there for cash deposits or convenience, while moving the bulk of their savings to earn a higher rate.

“This whole process — comparing, opening, and transferring — takes about 15 minutes. That’s less time than most people spend scrolling social media in a morning. The return on those 15 minutes? Potentially thousands of dollars over the next few years.”

Tools That Can Help You Save Smarter

You don’t need to be a financial expert to build wealth. You just need the right tools working in the background. Here are some worth exploring:

Sites like Bankrate and NerdWallet let you compare current APYs across dozens of accounts in real time. Use them every 6–12 months to make sure your rate is still competitive — banks adjust rates, and loyalty doesn’t always pay.

Tools like YNAB (You Need A Budget) or Copilot Money help you identify exactly how much you can realistically transfer to savings each month. If you’ve never tracked your spending, the results are often surprising — and motivating.

If you’re working toward bigger financial goals like buying a home, pairing your savings strategy with a credit monitoring tool (like Credit Karma or Experian) helps you build both pillars simultaneously. Learn more about your credit score ranges at credit score ranges.

Some banks and apps like Acorns automatically round up your everyday purchases and sweep the spare change into a savings or investment account. It’s a painless way to save money you won’t even miss.

If you’re just getting started comparing options, tools like Bankrate’s savings rate comparison tool can help you find the current best rates with no sales pressure and no account required.

Why You Haven’t Switched Yet (And Why That Needs to Change)

Be honest — have you been meaning to look into a high-yield savings account for a while but just haven’t gotten around to it? You’re not alone. There are a few very human reasons people put this off:

— it’s not. 15 minutes, one form, done.

— and you should keep trusting them for checking. But your savings deserve better.

— that’s exactly what the banks are counting on. Multiply the difference by your actual balance and the years you plan to save. Then decide if it matters.

— both account types carry the same FDIC insurance. Online banks aren’t riskier, they’re just more efficient.

Here’s the real talk: every day your money sits in a low-yield account, you’re effectively paying a “laziness tax” to your bank. You’re not doing anything wrong — you’re just not doing the one thing that would make a meaningful difference.

Loss aversion is a powerful motivator here: you’re not just missing out on gains — you’re actively losing purchasing power to inflation. If your savings account earns 0.10% and inflation runs at 2.5%, your money is shrinking in real terms every year.

“You don’t need to be a finance expert. You don’t need to take any risks. You just need to move your money to a better parking spot — one that pays you while you wait.”

Frequently Asked Questions

Final Thoughts: Your Money Should Be Working Harder

Here’s the bottom line: high-yield savings accounts build wealth faster because they pay you more for doing the same thing — saving money. There’s no catch, no complexity, and no risk trade-off. You’re just choosing a smarter place to park your cash.

The traditional savings account isn’t inherently bad. It’s just a product that was designed for a different era — one before online banking made it possible for anyone to access institutional-level savings rates from their phone in 15 minutes.

If you’re in your 20s or 30s, the compounding effect of starting now is enormous. If you’re in your 40s or 50s, there’s no better time than today to stop leaving money on the table. Even a few years of earning 4.75% instead of 0.10% adds up to thousands of dollars you’ll be glad you didn’t leave behind.

You work hard for your money. Make your money work harder for you.

“The switch takes 15 minutes. The difference over the next decade? Potentially thousands of dollars. That’s a pretty good return on a Tuesday afternoon.”

Next step: Search for ‘best high-yield savings accounts 2026,’ pick a FDIC-insured option with no fees, and open an account today. Your future self will thank you.

→ Roth 401(k) vs Roth IRA: Which One Actually Makes You Richer?

→ Treasury Bills (T-Bills) Explained: How to Invest Safely in 2026

→ Average 401(k) Return: What to Expect in 2026

→ How to Get Rich Young in 2026 (No BS, Just What Actually Works)

→ Best Investing Apps for Beginners

→ Capital Gains Tax Rates: What You Need to Know

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice. Interest rates mentioned are approximate figures for 2026 and are subject to change. Always verify current rates and FDIC insurance status before opening any financial account. Consult a qualified financial advisor for personalized guidance.