Your credit score is one of the most powerful three-digit numbers in your financial life — and most people have no idea what it actually means. Whether you just pulled your score for the first time and stared at the number wondering “Is this good?” or you’re preparing to apply for a mortgage, a car loan, or a new credit card, this guide explains everything.

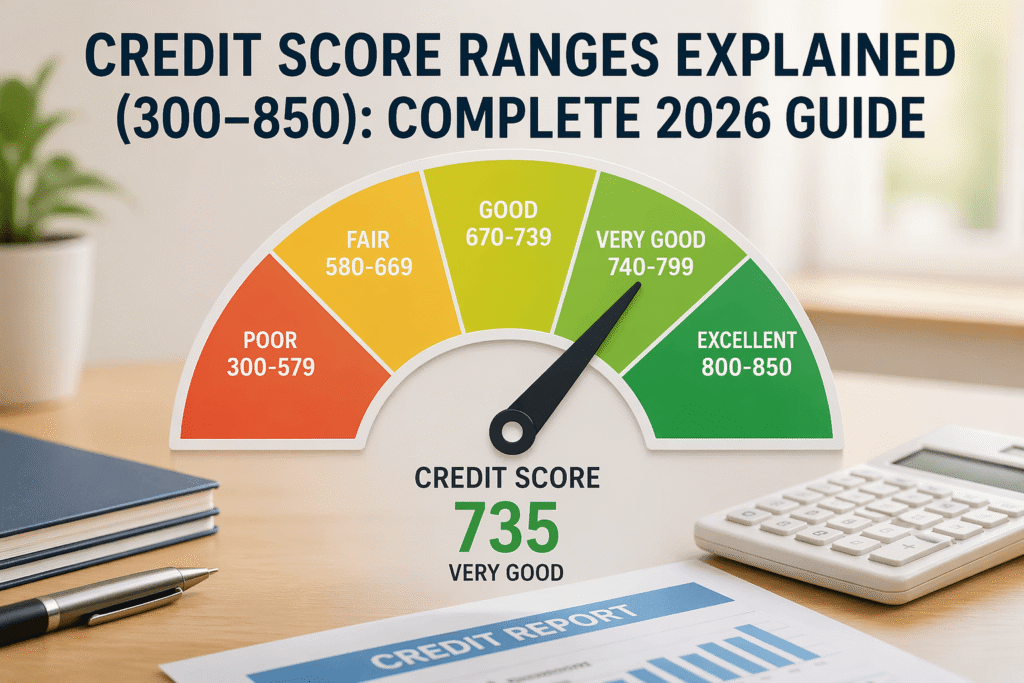

Credit scores in the U.S. range from 300 to 850. That’s the scale used by the two most widely used scoring models: FICO® Score and VantageScore. The higher your number, the less of a lending risk you appear to lenders — and the better the financial products, rates, and terms you can access.

In this guide, you’ll learn exactly what each score range means, how lenders interpret your number, what factors push your score up or down, and the most effective ways to improve it. Let’s break it all down.

What Is a Credit Score?

Think of your credit score as a financial reputation score. It tells lenders, landlords, and even some employers how responsibly you’ve handled borrowed money in the past — and how likely you are to pay your bills on time in the future.

Your score is calculated using information from your credit report — a detailed record of your credit history maintained by the three major credit bureaus: Experian, Equifax, and TransUnion. Lenders report your payment behavior to these bureaus every month, and scoring models analyze that data to produce your score.

Your credit score affects more of your life than most people realize. Here’s where it comes into play:

According to the Consumer Financial Protection Bureau (CFPB), credit scores are among the most commonly used tools in lending decisions across the country.

Credit Score Range (300–850): The Complete Breakdown

Both FICO and VantageScore use the 300–850 range, though the labels for each tier vary slightly between the two models. The table below uses the most widely recognized definitions, based on the myFICO scoring scale:

| Score Range | Rating | What It Means | Typical Lender View |

|---|---|---|---|

| 300–579 | Poor | High-risk borrower; most lenders decline | Likely declined; secured cards only |

| 580–669 | Fair | Below average; higher rates, limited options | Subprime loans; rates of 15–25%+ |

| 670–739 | Good | Acceptable; most lenders approve with decent rates | Approved for most products; 7–15% rates |

| 740–799 | Very Good | Low-risk; better rates & premium card offers | Strong approval odds; competitive rates |

| 800–850 | Excellent | Elite borrower; best rates & top-tier products | Best rates, highest limits, premium cards |

Now let’s dig into each range — what it looks like, why people land there, and what it means for your financial options.

300–579 Poor Credit

A score below 580 is considered poor by most lenders, and it’s where financial options get very limited, very fast.

Why do people end up here?

If you’re in this range, getting approved for an unsecured loan is difficult. Most traditional banks will decline your application outright. You may qualify for a secured credit card (where you put down a cash deposit), or a credit-builder loan from a credit union — both of which are useful tools for rebuilding.

580–669 Fair Credit

The fair credit range sits just above poor — and it’s where millions of Americans find themselves after a financial setback or a slow start to their credit journey.

In this range, you can get approved for some loans and credit cards, but you’ll pay for it through higher interest rates. Lenders see you as a “subprime” borrower — someone who represents higher risk than average.

What you can typically access with fair credit:

The good news? Moving from the 500s into the 600s is one of the most achievable improvements — and the financial difference it makes is real. Check out our guide to credit cards for fair credit to see which products are actually designed for this range.

670–739 Good Credit

A score in the 670–739 range puts you in “good” territory — which means most mainstream lenders are willing to work with you.

This is where your financial options open up significantly. You’ll generally qualify for:

If you’re in this range, it’s worth pushing into Very Good territory (740+) — the improvement in loan rates and card offers is often dramatic. Small changes, like paying down one credit card, can sometimes get you there faster than you’d expect.

740–799 Very Good Credit

Welcome to the very good range — where lenders start competing for your business. At this level, you represent a low-risk borrower, and financial institutions know it.

Here’s what opens up with a very good credit score:

According to FICO data, only about 46% of Americans have scores above 740 — so reaching this range puts you solidly above the national average.

800–850 Exceptional / Excellent Credit

Scores in the 800–850 range are elite. Less than 21% of Americans reach this level — and those who do enjoy real, measurable financial advantages.

With an exceptional credit score, you can expect:

How Lenders Use Your Credit Score

Understanding the ranges is one thing. Knowing how lenders actually use those numbers is what really matters.

When you apply for any credit product — a mortgage, car loan, credit card, or personal loan — lenders run what’s called a “hard inquiry” and pull your credit score. Based on that number, they make several key decisions:

Here’s a real-world illustration of what your score costs (or saves) on a 30-year, $300,000 mortgage:

| Credit Score | Est. Rate | Monthly Payment* | vs. Best Score |

|---|---|---|---|

| 760–850 | ~6.5% | $1,896/mo | $0 extra |

| 700–759 | ~6.7% | $1,933/mo | +$37/mo |

| 640–699 | ~7.1% | $2,011/mo | +$115/mo |

| 580–639 | ~7.8% | $2,153/mo | +$257/mo |

| Below 580 | May not qualify | — | — |

*Estimates are illustrative and based on general rate patterns. Check CFPB’s mortgage rate tool for current data.

Looking to take out a personal loan? Our complete guide to personal loans explains what lenders look for and how to get the best rate for your credit profile. If you’re comparing lenders, read our LendingTree review to see how a loan marketplace can surface better rates.

What Factors Affect Your Credit Score?

Your credit score isn’t random — it’s calculated using a specific formula. The FICO model (the most widely used) weighs five key factors, as outlined by myFICO:

| Factor | Weight | What It Means |

|---|---|---|

| Payment History | 35% | On-time payments are the single biggest factor |

| Credit Utilization | 30% | How much of your available credit you’re using |

| Length of Credit History | 15% | Older accounts signal experience to lenders |

| Credit Mix | 10% | Having cards, loans, mortgages shows versatility |

| New Credit Inquiries | 10% | Too many applications in a short time raises flags |

1. Payment History (35%)

This is the most important factor by far. Every time you pay a bill on time, it’s recorded. Every time you miss a payment by 30 days or more, it gets reported to the credit bureaus and can drop your score significantly — sometimes by 50–110 points for a single missed payment.

The fix is straightforward: set up autopay for at least the minimum payment on every account, so you never miss a due date.

2. Credit Utilization (30%)

This measures how much of your available credit you’re using. If you have a $10,000 credit limit and carry a $3,000 balance, your utilization is 30%. Most experts recommend keeping it below 30% — and ideally below 10% for the best scores.

Quick tip: if you have multiple cards, spreading your balance across them (rather than maxing one out) can improve your utilization rate.

3. Length of Credit History (15%)

The longer you’ve had credit, the better. This is why closing old credit cards — even ones you don’t use — can actually hurt your score. That old card you’ve had for 10 years is helping your average account age, which lenders like to see.

4. Credit Mix (10%)

Lenders like to see that you can manage different types of credit responsibly. Having a mix of credit cards (revolving credit) and installment loans (like a car loan or student loan) shows financial versatility.

5. New Credit Inquiries (10%)

Every time you apply for new credit, a hard inquiry is added to your report. One or two inquiries have minimal impact, but applying for several loans or cards in a short window can signal financial stress to lenders and drop your score temporarily.

Note: checking your own credit is a soft inquiry and does not affect your score at all.

How to Improve Your Credit Score: 8 Proven Strategies

Good news: your credit score is not permanent. It changes based on your behavior — which means you have the power to improve it. Here are the most effective strategies:

Get your free credit reports at AnnualCreditReport.com — the only federally authorized source for free reports from all three bureaus.

For a deeper dive, see our full guide: How to Improve Your Credit Score Fast.

How Long Does It Take to Improve Your Credit Score?

This depends entirely on where you’re starting from and what’s dragging your score down. Here’s a realistic timeline:

| Timeframe | Action | Potential Gain |

|---|---|---|

| 30 days | Pay down high card balances | 10–40 points |

| 1–3 months | Consistent on-time payments | 20–60 points |

| 6–12 months | Dispute errors + lower utilization | 50–100 points |

| 1–2 years | Rebuild after missed payments | 100–150 points |

| 2–7 years | Recover from major negatives (bankruptcy, collections) | Full rebuild possible |

There’s no magic shortcut. Be wary of any company promising to “fix” your credit overnight — these are often credit repair scams. The CFPB warns consumers that no one can legally remove accurate negative information from your credit report before it naturally expires.

Most negative marks (late payments, collections) stay on your report for 7 years. Bankruptcies can remain for up to 10 years. But their impact on your score diminishes over time, especially if you’re building positive history on top of them.

Common Credit Score Myths — Debunked

Credit scores are surrounded by misinformation. Here are the myths that cause real financial damage:

How to Check Your Credit Score for Free

You have multiple options for monitoring your credit score without paying a cent:

For a full walkthrough of every free option available to you, read our guide: How to Check Your Credit Score for Free.

Which Credit Cards Match Your Score Range?

Your credit score range largely determines which credit cards you’ll actually qualify for. Here’s a quick overview:

Final Thoughts: Your Credit Score Is Not Your Financial Destiny

A credit score — whether it’s 300 or 800 — is not a permanent label. It’s a snapshot of your credit behavior up to this point, and it changes every single month based on what you do next.

The most important thing to understand is this: small, consistent habits have a bigger impact than dramatic one-time actions. Paying on time every month, keeping balances low, and avoiding unnecessary new applications will move your score in the right direction — sometimes faster than you’d expect.

If you’re just starting out, the path from Poor to Fair is achievable in months. From Fair to Good in another year. And once you’re in the Good range, the distance to Very Good or Excellent is closer than it looks.

The financial rewards of a high credit score are real and significant — lower interest rates, better products, more negotiating power, and less money lost to fees and high-rate debt. Every point you gain is a step toward a stronger financial future.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Credit scoring models vary by lender and bureau. Consult a qualified financial professional for advice tailored to your situation.