⚡ Quick Answer

A CD ladder is a savings strategy where you split your money across multiple CDs with different maturity dates — like 1, 2, 3, 4, and 5 years — so you always have cash becoming available while still locking in higher long-term rates. It takes about 30 minutes to set up and gives you the best of both worlds: solid returns without tying all your money up for years at a time.

By FinanceNavigatorPro Editorial Team | Updated June 2026 | 15 min read

📋 Quick Summary

- ✓A CD ladder splits your savings across multiple CDs with staggered maturity dates (1–5 years)

- ✓You get higher rates than a savings account while keeping regular access to your money

- ✓In 2026’s falling-rate environment, laddering locks in today’s still-decent rates before they drop further

- ✓A $20,000 CD ladder could earn roughly $2,500+ in interest over five years

- ✓You only need $500–$1,000 to start — no six-figure nest egg required

- ✓The best banks for CD laddering right now include online banks like Marcus, Ally, and Discover

- ✓Reinvesting matured CDs at the longest term keeps your ladder growing automatically

Okay, real talk: have you ever had $15,000 sitting in a savings account earning a lousy 0.5% interest and thought, “there has to be a better way”? You’re not wrong. There is.

But then you look at CDs and think — “what if I need the money in two years? I don’t want to lock everything up for five years.” Totally valid concern.

That’s exactly why the CD ladder strategy exists. It’s the middle ground between the flexibility of a high-yield savings account and the higher returns of long-term CDs. And once you understand how it works, you’ll wonder why you didn’t set one up sooner.

Let’s walk through everything — step by step, plain English, real numbers.

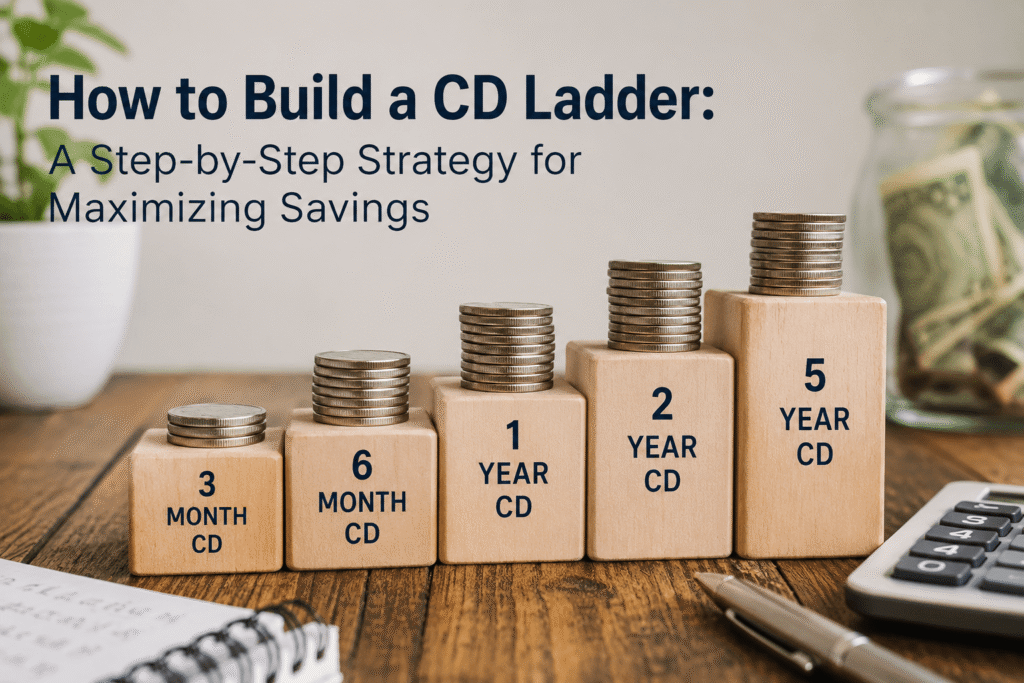

What Is a CD Ladder? (The 60-Second Explanation)

A CD ladder is exactly what it sounds like — you build a “ladder” with multiple CDs, each one representing a rung. Every rung has a different maturity date.

Here’s the basic idea: instead of putting $20,000 into a single 5-year CD (and locking it all up), you split it into five $4,000 CDs with terms of 1, 2, 3, 4, and 5 years.

Every year, one CD matures. You take that money, reinvest it into a new 5-year CD, and the cycle continues. You always have a CD maturing soon — which means you’re never truly locked out of your own savings.

Think of it like a garden. You’re not planting all your seeds on the same day hoping they all bloom at once. You stagger them so something is always ready to harvest.

The result? You capture the higher rates of longer-term CDs while maintaining regular access to your cash — without penalty fees.

Why CD Laddering Makes Especially Good Sense in 2026

Here’s the honest situation with interest rates right now: we’re in a slow, gradual descent from the 2023–2024 peak. The Federal Reserve raised rates aggressively back then, which pushed CD rates to the best levels we’d seen in nearly two decades. Now? Rates are still solid — but they’re trending down.

So what does that mean for you?

- •If you park everything in a short-term CD, you’ll keep rolling it over at lower and lower rates as they drop

- •If you lock everything in a 5-year CD right now, you capture today’s rate — but lose all flexibility

- •If you build a ladder, you lock in today’s still-competitive rates on the longer rungs while keeping shorter rungs available for reinvestment

The CD ladder is built for exactly this kind of environment. You’re not betting on rates going up or down. You’re hedging. Smart move.

💡 Pro Tip

With rates trending down in 2026, weighting your ladder toward longer terms (3–5 years) lets you lock in higher rates now before they potentially fall further. We’ll talk about how to do this in the strategy section.

How a CD Ladder Works: A Visual Walk-Through

Year One — Building Your Ladder

Let’s say you’ve got $20,000 to work with. Here’s what year one looks like if you split it into five equal rungs:

| Rung | Term | Amount | Est. APY | Matures | Interest |

|---|---|---|---|---|---|

| 1 | 1-Year | $4,000 | 4.50% | Jun 2027 | ~$180 |

| 2 | 2-Year | $4,000 | 4.25% | Jun 2028 | ~$350 |

| 3 | 3-Year | $4,000 | 4.10% | Jun 2029 | ~$515 |

| 4 | 4-Year | $4,000 | 4.00% | Jun 2030 | ~$666 |

| 5 | 5-Year | $4,000 | 3.90% | Jun 2031 | ~$820 |

| Total | $20,000 | Avg ~4.15% | ~$2,531 |

Note: APY estimates are illustrative and based on competitive online bank rates as of mid-2026. Always verify current rates before opening accounts.

Year Two and Beyond — The Reinvestment Magic

When Rung 1 matures in June 2027, you don’t just cash out and spend it (unless you need to — that’s the beauty of it). Instead, you roll it into a new 5-year CD. Now you’ve got a $4,000 5-year CD running alongside the others.

Every year after that, another rung matures, you reinvest at the 5-year rate, and within five years, your entire ladder is running at maximum-term rates. Meanwhile, you always have a CD coming due every 12 months.

It’s a self-sustaining machine that builds on itself.

Step-by-Step Guide: How to Build a CD Ladder

Decide How Much You’re Laddering

Before you open any accounts, figure out your total. This is money you genuinely don’t need for everyday expenses. Think of it as your “medium-term” savings — not your emergency fund (keep that liquid), and not money you’re investing in the market.

Common starting amounts:

- •$5,000 minimum to make it worth your time across multiple banks

- •$10,000–$25,000 is the sweet spot for most people

- •$100,000+ works too — just watch FDIC limits (more on that below)

Keep your emergency fund separate. A good rule of thumb: 3–6 months of expenses in a high-yield savings account, then ladder the rest.

Choose Your Ladder Terms (Your Rungs)

The classic CD ladder uses 1, 2, 3, 4, and 5-year terms — one rung per year. But you can customize this based on your situation:

- •Classic 5-Rung Ladder: 1/2/3/4/5 year — best for long-term savers who want set-it-and-forget-it

- •Short-Term Mini Ladder: 3/6/9/12-month — good if you want maximum flexibility or rates are falling fast

- •Barbell Strategy: Heavy on short (6-month) and long (5-year), skipping the middle — works when the yield curve is unusual

- •3-Rung Starter Ladder: 1/2/3 year — great if you’re new to CDs and want to test the waters

In 2026, with rates easing down gradually, most financial experts lean toward the classic 5-rung or even weighting more toward longer terms. Locking in that 3.75%–4.5% range on 4–5 year CDs could look really smart 18 months from now.

Find the Best CD Rates (Don’t Use Your Regular Bank)

This is where most people leave money on the table. Your local bank or national chain bank almost certainly offers terrible CD rates. We’re talking sometimes 0.05% compared to the 4%+ you can get online.

Where to actually shop:

- •Online banks (Marcus by Goldman Sachs, Ally Bank, Discover Bank, Synchrony) — consistently offer the best rates

- •Credit unions — often match or beat online banks, especially for members

- •Brokered CDs through Fidelity or Vanguard — good for large amounts, though terms differ

Don’t feel like you have to use the same bank for every rung. Spread across two or three institutions if one bank has a better rate on a particular term. And always verify rates are FDIC-insured (or NCUA for credit unions).

FDIC Limit Reminder

Each depositor is insured up to $250,000 per bank. If you’re laddering $200,000+, split across multiple institutions to stay protected.

Open Your CDs and Set Maturity Reminders

Once you’ve found your rates and chosen your banks, opening a CD is usually straightforward — most online banks can do it in 10–15 minutes per account.

A few things to do when you open each CD:

- •Note the exact maturity date — put it in your calendar, phone, and a spreadsheet

- •Understand the early withdrawal penalty — typically 90–180 days of interest; know what you’d lose if you had to break it

- •Check the auto-renewal policy — many banks automatically roll your CD into the same term if you don’t act. That could trap you at whatever rate is available at maturity.

- •Set a reminder 2 weeks before maturity — gives you time to compare rates and decide whether to reinvest or redirect

Reinvest Matured CDs at the Longest Term

This is the engine that keeps your ladder running. When a CD matures, your default move should be to reinvest at the longest available term — typically 5 years — unless you have a specific reason not to.

But life happens, and that’s the whole point of the ladder. If a CD matures and you need the cash for a home repair, car payment, or whatever — take it. No penalty, no stress. That’s what the ladder was designed to handle.

If you don’t need the cash? Roll it over. Give it 5 more years to grow. Let compounding do its thing.

Real-Life CD Ladder Examples

The $10,000 Beginner Ladder

📖 Real Example

Meet Sarah. She’s 42, has $10,000 sitting in a savings account earning basically nothing, and recently read that CD rates are still decent. She doesn’t need this money anytime soon, but she’d feel better knowing she could access some of it if she had to.

Sarah builds a 5-rung ladder with $2,000 per rung across terms of 1–5 years. In year one, she earns roughly $335 in interest across all five CDs. By year five, she’s got a fully mature ladder earning $500+ per year — and she’s never been more than 12 months away from accessing $2,000 penalty-free.

The $50,000 Near-Retirement Ladder

📖 Real Example

Then there’s Mike, 59, who just rolled over an old 401(k) into an IRA and wants to keep $50,000 in something conservative for the next several years. He’s not trying to beat the stock market. He just doesn’t want to lose it.

Mike builds a 5-rung ladder with $10,000 per rung. Over five years, he earns over $10,000 in total interest — with $10,000 becoming available every year like clockwork. When he turns 65 and starts drawing down, the ladder is already timed to release funds right when he needs them.

CD Ladder Strategy in a Falling Rate Environment

“But wait — if rates are falling, why would I lock into a CD now?”

Great question. Here’s the counterintuitive answer: a falling-rate environment is actually one of the best times to use a CD ladder — specifically because locking in a portion of your savings at today’s higher rates protects you from rate drops.

Think of it this way. If you keep everything in a high-yield savings account and rates drop from 4.5% to 2.5% over the next two years — your interest drops immediately. Zero protection.

But if you ladder and lock 60% of your savings into 3–5 year CDs at 4%+, that portion keeps earning 4% even as new-account rates fall. You’re not stuck — the shorter rungs still mature and give you flexibility — but the longer ones protect your yield.

Falling-Rate Ladder Adjustments to Consider

- •Weight longer rungs more heavily — instead of equal splits, put 30–40% in the 4–5 year CDs

- •Consider no-penalty CDs for short-term rungs — these let you break out early without fees if something changes

- •Lock in NOW rather than waiting — every month you delay could mean locking in at a lower rate

CD Ladder vs. Your Other Savings Options

Should you do a CD ladder, stick with a high-yield savings account, or try Treasury bills? Here’s an honest comparison:

| Factor | CD Ladder | Single CD | HYSA | T-Bills |

|---|---|---|---|---|

| Liquidity | Medium | Low | High | Medium |

| Rate Lock | Partial | Full | None | Short-term |

| Rate Risk | Spread out | High | Fully exposed | Low |

| Setup Effort | Moderate | Easy | Easy | Moderate |

| FDIC Protected | Yes | Yes | Yes | No (Treasury) |

| Min Investment | $500–$1K | $500 | $0 | $100 |

| Best For | Balanced savers | Rate chasers | Short-term | Inflation hedge |

The takeaway? CD laddering sits in a sweet spot. It’s not as flexible as a HYSA but earns more. It’s not as complex as T-bills but offers better liquidity than a single long-term CD. For most savers with a 3–10 year horizon, it’s hard to beat.

Common Mistakes to Avoid When Building a CD Ladder

Mistake #1: Using Your Emergency Fund

Your emergency fund is not CD material. It needs to be liquid — sitting in a HYSA or money market account, ready to go. Putting it in CDs (even short-term ones) creates a situation where a real emergency forces you to break a CD and pay penalties. Keep them separate.

Mistake #2: Ignoring Auto-Renewal Policies

This catches a lot of people off guard. Your CD matures, you forget to act, and the bank automatically rolls it into a new CD at whatever rate is available. Sometimes that’s fine. But if rates have dropped significantly, you’ve just locked yourself in at a lousy rate without realizing it. Always set reminders and review before auto-renewal kicks in.

Mistake #3: Not Shopping Around

Your local bank is probably not offering competitive rates. A half-percent difference doesn’t sound like much, but on $20,000 over five years, it can mean hundreds of dollars of lost interest. Take 30 extra minutes to compare rates on Bankrate or DepositAccounts before committing.

Mistake #4: Breaking CDs Early for Non-Emergencies

Breaking a CD early to take advantage of a slightly higher rate elsewhere rarely makes mathematical sense. The early withdrawal penalty (often 90–180 days of interest) almost always wipes out the rate advantage. Unless you’ve genuinely hit a financial emergency, let the rungs mature naturally.

Mistake #5: Building a Ladder That’s Too Short

A 1-year and a 2-year CD is not really a ladder — it’s just two CDs. To get the real benefits of laddering (regular access plus long-term rate exposure), you need at least three rungs, ideally five. Don’t shortchange yourself on the setup.

Frequently Asked Questions

Can I build a CD ladder with just $1,000?

Yes, technically — but it’s tight. With $1,000 across five CDs, you’re only putting $200 per rung, and many banks have minimum deposits of $500–$1,000 per CD. A better approach with $1,000 is to build a 2-rung mini ladder (6-month + 12-month) and expand from there as your savings grow.

What is a mini CD ladder and is it worth it?

A mini CD ladder uses shorter terms — think 3, 6, 9, and 12-month CDs — instead of the traditional 1–5 years. It’s great when you think you might need the money sooner, or when short-term CD rates are unusually high compared to long-term ones (as happened in 2023). The tradeoff: you’ll need to reinvest more frequently and keep a closer eye on your rates.

Should I use the same bank for all my CD rungs?

Not necessarily. Using the same bank is convenient — one login, one dashboard — but you might leave money on the table. If Ally has the best 1-year rate and Marcus has the best 5-year rate, use both. Just make sure you track maturity dates carefully across banks. A simple spreadsheet works perfectly.

What happens if I need money before a CD matures?

You have two options: pay the early withdrawal penalty (usually 90–180 days of interest, which hurts but isn’t devastating) or, if you planned ahead, tap the CD rung that’s closest to maturity and only take the hit on a small portion. This is exactly why the staggered structure exists — you’re rarely more than 12 months from a penalty-free maturity.

Are CD ladders worth it in 2026?

Honestly? Yes — more than they were in 2020 when CD rates were essentially zero. With top online bank rates still ranging from 3.75% to 4.75% depending on term, a 5-year ladder built today could lock in solid returns before rates potentially fall further. It’s not going to make you rich, but for money you want safe, predictable growth on? It’s one of the smartest low-risk moves available right now.

How is a CD ladder different from a bond ladder?

Both concepts are similar — you stagger maturity dates across multiple instruments to manage rate risk and maintain liquidity. But CDs are FDIC-insured and issued by banks, while bonds are debt instruments that can fluctuate in value before maturity and carry more complexity. For most everyday savers, CDs are the simpler, safer option.

Final Thoughts: Is the CD Ladder Right for You?

If you’ve got savings sitting in a regular bank account, or even a high-yield savings account, and you know you won’t need all of it in the next 12 months — the CD ladder is worth serious consideration.

It’s not complicated. It doesn’t require a financial advisor. You don’t need six figures to start. What it does require is a little upfront planning (an afternoon, honestly) and the discipline to let the money sit and grow.

The 2026 rate environment is exactly the kind of moment the CD ladder was built for — decent rates still available, but uncertainty about where things go from here. Locking in a portion of your savings at today’s rates, while keeping regular access to portions of it, is just smart financial hygiene.

Start small if you’re nervous. Build a $5,000 three-rung ladder. See how it feels. Then expand from there.

Your future self — the one watching CDs mature every year like clockwork and reinvesting at whatever rate makes sense then — will absolutely thank you.

Ready to get started? Compare the best CD rates at top online banks to find the right rates for each rung of your ladder.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. CD rates and terms change frequently — always verify current rates with individual banks before opening accounts. FDIC insurance limits apply. Consult a qualified financial advisor for personalized guidance.

Related Reading