Solvency means your total assets are worth more than your total debts — you’re financially above water. Insolvency is the opposite: your liabilities exceed what you own, or you can no longer pay your bills as they come due. The difference matters because insolvency can spiral into damaged credit, legal action, and even bankruptcy if left unchecked — while staying solvent gives you options, stability, and peace of mind.

What Is Solvency?

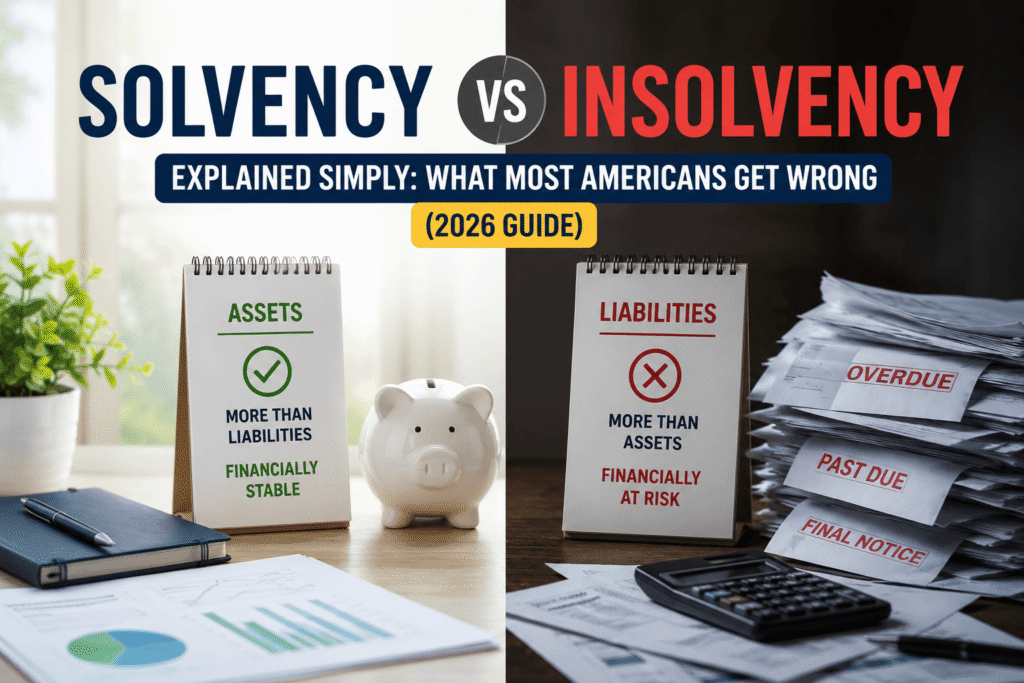

Solvency is simply this: you own more than you owe.

More precisely, a person or business is considered solvent when their total assets — everything of value they own — exceed their total liabilities, which is all the money they owe to others.

That’s it. No complicated formula needed.

Here’s the basic equation:

Assets include things like: your savings account balance, your home’s current market value, retirement accounts (401k, IRA), vehicles, investments, and any other property of value. Liabilities include mortgage balance, credit card debt, student loans, car loans, medical bills, and any other money you owe.

A Real-Life Example of Solvency

Meet Sarah. She’s 34, lives in Ohio, and has:

Even if she hit a rough patch — a medical emergency, a layoff — she has a financial cushion to fall back on.

Solvency vs. Liquidity: Don’t Confuse These

Here’s something most people get confused: you can be solvent but still cash-strapped. That’s called a liquidity problem.

Imagine you have $400,000 in home equity but only $200 in your checking account and a $2,000 car payment due tomorrow. You’re technically solvent — your assets far outweigh your debts — but you’re illiquid. Your wealth isn’t accessible quickly enough to cover your immediate obligations.

True financial health means being both solvent AND having solid cash flow. One without the other creates vulnerabilities.

What Is Insolvency?

Insolvency is the financial condition where a person or business cannot meet their debt obligations — either because their debts exceed their assets, or because they simply don’t have enough cash coming in to pay their bills on time.

There are actually two types of insolvency, and understanding both matters:

Your total liabilities exceed your total assets. Your “net worth” is negative. Example: You owe $120,000 across credit cards, car loan, student loans, and medical debt — but your total assets only add up to $80,000. That $40,000 gap? That’s balance sheet insolvency.

Your assets may technically exceed your debts, but you can’t pay bills as they come due because cash isn’t flowing in fast enough. This one catches people off guard — you might have solid retirement accounts and home equity, but if your monthly take-home doesn’t cover bills, you’re cash-flow insolvent.

The Emotional Reality of Insolvency

Let’s be honest: insolvency isn’t just a spreadsheet problem. It’s stressful. It shows up as 3 a.m. anxiety, avoiding opening the mail, letting your phone go to voicemail because you don’t recognize the number. According to the Consumer Financial Protection Bureau (CFPB), financial stress is one of the leading contributors to relationship strain and mental health challenges in American households.

The good news? Insolvency is a financial state, not a permanent identity. Millions of Americans have dug out from under serious debt. The key is recognizing it early and taking action.

Solvency vs Insolvency: The Core Differences

Here’s a side-by-side breakdown of how solvency and insolvency compare across every dimension that matters in real life. Use this as a quick reference:

| Factor | ✅ Solvency | ⚠️ Insolvency |

|---|---|---|

| Definition | Assets exceed liabilities | Liabilities exceed assets |

| Financial Health | Stable or growing | Declining or at risk |

| Cash Flow | Positive or manageable | Negative or tight |

| Debt Level | Manageable relative to assets | Exceeds ability to repay |

| Credit Score | Generally healthy (670+) | Often falling or damaged |

| Risk Level | Low to moderate | High — legal action possible |

| Loan Approval | Usually approved | Often denied or high-rate only |

| Real-Life Signal | Bills paid on time, savings growing | Missing payments, calls from collectors |

| Legal Exposure | None under normal conditions | Creditor lawsuits, bankruptcy possible |

Why This Actually Matters in Real Life

You might be thinking: “Okay, I get the definition — but why should I care about this specific distinction?” Here’s the deal: whether you’re solvent or insolvent affects nearly every major financial decision and opportunity in your life.

Credit bureaus don’t label you “insolvent” directly — but they track all the behaviors that go along with it. Missed payments, maxed-out credit cards, accounts in collections, and court judgments all drag your score down. The Federal Reserve’s research shows that households with negative net worth are far more likely to struggle with access to credit at competitive rates. A damaged credit score doesn’t just make borrowing harder — it can affect your ability to rent an apartment, get certain jobs, and even secure some insurance policies. Learn more about credit score ranges and what they mean for your financial life.

Lenders look at your debt-to-income ratio and your assets when you apply for a mortgage, car loan, or personal loan. If you’re insolvent or on the edge, you’re either denied outright or offered rates so high that the loan makes your financial situation worse. Think about what that means in practice: you want to buy a home, use our mortgage payment calculator to plan the numbers, and then find out that your financial condition means you either don’t qualify or you’re looking at an interest rate two or three points higher than someone with a clean balance sheet. Over a 30-year mortgage, that difference can cost you $50,000 to $100,000+.

Here’s where things get serious. If you’re insolvent and stop paying creditors, those creditors don’t just shrug and walk away. They can:

The Federal Trade Commission (FTC) has consumer protections around debt collection, but those protections don’t make the debt disappear. Understanding your status before things escalate gives you far more options.

Financial insolvency bleeds into everyday life. It affects how you sleep, how you interact with your family, and how clearly you think at work. There’s nothing abstract about it. Studies consistently show that financial stress is one of the most disruptive forces on cognitive performance and mental health. Solvency, by contrast, creates psychological breathing room. Even if you’re not wealthy, knowing that your assets outweigh your debts and your bills are covered creates a stability that changes how you experience daily life.

Real-Life Examples: Solvency and Insolvency in Action

Let’s get practical with some real scenarios you might recognize.

Warning Signs You’re Heading Toward Insolvency

Most people don’t wake up one day and suddenly find themselves insolvent. It’s a gradual slide. Here are the red flags that something is wrong:

You’re only making minimum payments on your credit cards — this means your balance is growing every month, not shrinking

Your debt-to-income ratio exceeds 43% — this is the standard threshold lenders use to flag “high risk” borrowers, per CFPB guidelines

You’re using credit to cover basic living expenses — groceries, utilities, gas — not just occasional big purchases

You’ve missed at least one bill payment in the last 90 days

Your savings account balance is trending toward zero despite earning a regular income

You’ve received calls or letters from collection agencies

You’re borrowing from one source to pay another (credit card to pay credit card, or payday loan to make rent)

Insolvency vs Bankruptcy: What’s the Actual Difference?

People use these terms interchangeably, but they’re not the same thing — and the distinction matters.

The state of being unable to pay your debts. It can be temporary or chronic. Many people navigate out of insolvency without ever going to court.

The formal legal process — filed in federal court — that gives you either a structured way to repay debt (Chapter 13) or discharge certain debts entirely (Chapter 7). You generally must be insolvent to qualify.

Many insolvent people never file for bankruptcy. They work out payment plans with creditors, consolidate debt, negotiate settlements, or simply grind through until their financial position improves. According to Cornell Law School’s Legal Information Institute, bankruptcy is a federal process governed by Title 11 of the U.S. Code — and it has significant long-term consequences, including staying on your credit report for 7–10 years.

Bankruptcy isn’t shameful — it exists precisely because people hit financial walls they can’t get through on their own. But it should be a last resort after exhausting other options, and you should always consult a qualified attorney before filing.

How to Stay Solvent — or Recover If You’re Not

This is where we stop diagnosing and start fixing. Whether you’re comfortably solvent and want to stay that way, or you’re currently struggling and looking for a way out, these steps work.

The first step is always clarity. Pull up every account, every loan balance, every credit card statement. Write it down or use a spreadsheet. Calculate your total assets and total liabilities right now. Most people who end up insolvent never did this exercise — they avoided it because they were afraid of what they’d find. That avoidance is expensive.

Know exactly what comes in and what goes out. Not a rough estimate — exact numbers. Your bank and credit card statements have everything you need. If more is going out than coming in, you have a cash flow problem that needs addressing before anything else.

Credit card interest rates average over 20% APR in the U.S. right now. Every month you carry a balance, you’re losing ground. Prioritize paying off your highest-interest debt first (avalanche method) or the smallest balance first for psychological momentum (snowball method). Consider a balance transfer card with a 0% introductory period, or a personal loan at a lower rate to consolidate. Learn more about how to avoid credit card debt and how to pay debt in collections.

Here’s where most people skip ahead and end up back in trouble: you can’t sustainably pay down debt if one unexpected expense sends you right back to the credit card. Even $1,000 in a dedicated emergency account creates a buffer. Aim for 3–6 months of living expenses over time, but start small and build consistently.

Good budgeting and credit monitoring tools take the manual work out of staying on track. A solid credit monitoring service will show your score, flag changes, and help you understand what’s affecting your financial health. If you’re managing debt, budgeting apps can automate the tracking so you’re not relying on willpower alone. Tools like these give you a clear, real-time snapshot of whether you’re moving toward solvency or away from it.

If you’re in serious debt, you have more options than you might think: debt management plans through nonprofit credit counseling agencies, direct negotiation with creditors, debt consolidation loans, and settlement offers. The CFPB’s debt relief resources are a good starting point for understanding what’s available and what to watch out for.

There’s no medal for struggling alone. A certified financial planner (CFP), a nonprofit credit counselor, or a bankruptcy attorney can give you a clear picture of your options. Many nonprofit agencies offer free or low-cost counseling. The National Foundation for Credit Counseling (NFCC) is a vetted nonprofit network that connects Americans with accredited counselors at little to no cost.

How to Calculate Your Solvency Ratio

If you want a more precise measure than just “assets minus liabilities,” you can use the solvency ratio:

For example:

| Assets | Liabilities | Ratio | Status |

|---|---|---|---|

| $200,000 | $80,000 | 2.5 | ✅ Comfortably solvent |

| $150,000 | $150,000 | 1.0 | ⚡ Break even (vulnerable) |

| $50,000 | $55,000 | 0.91 | ⚠️ Technically insolvent |

A ratio of 1.5 or higher is generally considered a comfortable safety margin for individuals. For businesses, lenders and investors often look for ratios of 1.5 to 2.0+. To track your mortgage’s impact on this ratio over time, try our mortgage payment calculator — it shows you exactly how each payment builds equity and reduces your liability, moving your solvency ratio in the right direction.

Solvency and Your Credit Score: The Connection

Your credit score and your solvency are deeply intertwined — though they’re measuring slightly different things.

Your credit score (whether FICO or VantageScore) primarily tracks your payment history, credit utilization, length of credit history, and types of credit. Your solvency status is about your total balance sheet. But they influence each other constantly.

When you’re insolvent, the behaviors that follow — missing payments, maxing out cards, having accounts sent to collections — directly and severely damage your credit score. And a low credit score makes it harder to access the affordable credit you might need to climb out of insolvency (lower-rate debt consolidation loans, for instance).

Conversely, improving your solvency by paying down debt and building assets naturally leads to credit score improvements over time. The two metrics move together. If you’re working on repairing your credit while addressing insolvency, check out our guides on how to raise your credit score fast, remove late payments from your credit report, and how to remove negative items from your credit report.

Special Situations: Student Loans, Medical Debt, and Mortgages

Not all debt is created equal, and how different types of debt affect your solvency — and what you can do about them — varies significantly.

Student Loans

Student loan debt is unique because it generally can’t be discharged in bankruptcy (with some narrow exceptions), has specific income-driven repayment options, and may qualify for forgiveness programs. The Department of Education’s Federal Student Aid office is the definitive resource for understanding your repayment and forgiveness options. If student loans are pushing you toward insolvency, income-driven repayment (IDR) plans can dramatically reduce your monthly obligation and free up cash flow. See also our guide on subsidized vs unsubsidized student loans.

Medical Debt

Medical debt is the leading cause of personal bankruptcy in the United States. If you’re carrying significant medical debt, know that hospitals and healthcare systems typically have financial hardship programs that are not widely advertised. Ask your provider directly. Many bills are negotiable, and nonprofit hospitals are required by law to offer charity care programs.

Mortgage Debt

Your mortgage is likely your largest liability — and your largest asset if you have equity. The key is understanding whether your mortgage is sustainable relative to your income and total debt load. A debt-to-income ratio above 43% (including your mortgage payment) is typically where lenders and financial planners start flagging risk. Use our mortgage payment calculator to model your payment scenarios and see how refinancing or extra payments affect your overall debt load over time. Also see our guide on refinancing a mortgage.

A Quick Note on Business Solvency

Everything we’ve covered applies to individuals, but businesses face the same fundamental dynamic. A business is solvent when its assets exceed its liabilities. The difference is that business insolvency has formal legal pathways beyond personal bankruptcy:

The business liquidates its assets to pay creditors and ceases operations.

The business restructures its debts and continues operating under court supervision — often used by large corporations.

Similar to personal Chapter 13 for business owners who are personally liable for business debts.

Small business owners should also know that personal liability depends heavily on business structure. An LLC or corporation generally protects personal assets from business debts — a sole proprietorship does not. This is one of many reasons why proper business structure matters from day one.

Frequently Asked Questions

Here are the most common questions people have about solvency and insolvency — answered in plain English:

Yes — and this is more common than people think. You can technically be solvent (assets > liabilities) but have poor cash flow. If most of your wealth is tied up in a home or retirement account and your monthly income barely covers bills, you might feel broke even though you’re technically above water.

Insolvency is the financial condition — your debts outweigh your assets or you can’t pay bills as they come due. Bankruptcy is the legal process you might go through as a result of insolvency. Not every insolvent person declares bankruptcy, and not every bankruptcy filer was technically insolvent on paper.

Add up everything you own (savings, car, home equity, investments). Then add up everything you owe (credit cards, loans, mortgage balance). If your debts are larger than your assets, you’re balance-sheet insolvent. If you’re constantly unable to pay bills on time regardless of your net worth, that’s cash-flow insolvency.

Absolutely. Insolvency is a financial state, not a life sentence. Many people have climbed out of insolvency through disciplined budgeting, debt consolidation, negotiating with creditors, and increasing income. The sooner you address it, the more options you have.

Yes — significantly. Missing payments, high credit utilization, collection accounts, and legal judgments all damage your score. A FICO score below 580 is considered poor, and insolvency-related behavior is a major driver of score drops. The good news: credit scores can recover with consistent positive behavior over time.

No. Almost everyone has some debt — mortgages, car loans, student loans. Being in debt is normal. Insolvency is specifically when your total debt exceeds your total assets OR when you can no longer meet financial obligations as they come due. Debt becomes a problem when it’s unmanageable.

Yes. A business can continue operating while technically insolvent, especially if it has ongoing cash flow from operations. However, continuing to operate while insolvent can expose business owners to legal liability, particularly if they take on new debt they can’t repay.

Final Thoughts: Awareness Is Your Most Powerful Financial Tool

At the end of the day, solvency isn’t about being rich. It’s about being in control.

Millions of Americans are walking around with no clear picture of whether their total debts exceed their total assets — or whether the gap between their income and expenses is quietly widening every month. That’s not a moral failing. That’s the result of a financial education system that never taught this stuff clearly.

But now you know. And knowing is the entire first step.

If you’re comfortably solvent: protect it. Keep your debt manageable, build your emergency fund, and invest in assets that appreciate over time. Small consistent actions compound dramatically over years.

If you’re insolvent — or close to it: take a breath. This is fixable. Start with clarity (know your exact numbers), then move to cash flow (stop the bleeding), then tackle the debt. You don’t have to solve everything at once. You just have to start.

Grab a piece of paper (or a spreadsheet) and list your total assets and total liabilities right now. Calculate your solvency ratio. Whatever that number is — it’s just data. And data is something you can work with.

Disclaimer: This content is for informational purposes only and does not constitute financial, legal, or tax advice. Always consult with a qualified financial professional before making financial decisions. Finance Navigator Pro is not a licensed financial advisor.