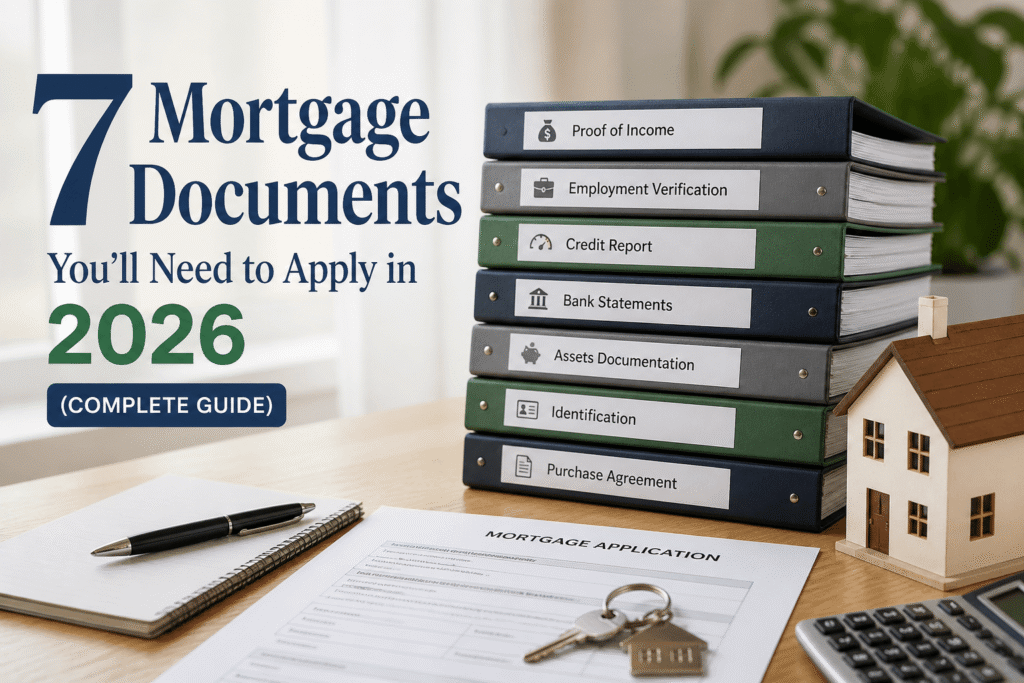

📋 Quick Summary: The 7 Mortgage Documents You’ll Need

Here’s a fast snapshot before we dive into the details:

Why Do Lenders Ask for All These Documents?

Here’s a question a lot of first-time buyers ask: “Why does my bank need all of this? They already know who I am.” It’s a fair point — but mortgage lending is a whole different world from opening a checking account.

When a lender approves your mortgage, they’re agreeing to lend you hundreds of thousands of dollars over 15 to 30 years. That’s an enormous amount of risk. Every document they request is their way of answering one core question: Can this person consistently repay this loan?

Think of it this way — if a friend asked to borrow $50, you’d probably hand it over without much thought. But if they asked to borrow $350,000? You’d want to see some proof they could pay you back. That’s exactly what lenders are doing.

Lenders are also legally required to follow strict underwriting guidelines set by government-backed entities like Fannie Mae and Freddie Mac, as well as federal regulations under the Dodd-Frank Act. These rules require lenders to verify your ability to repay — they can’t just take your word for it.

Beyond risk and regulation, documentation also protects you. Lenders who skip verification steps often end up issuing loans that borrowers can’t actually afford — which is part of what caused the 2008 housing crisis. Thorough documentation is a safeguard for everyone involved.

The 7 Mortgage Documents You’ll Need — Explained

Document #1: Proof of Income (Pay Stubs & W-2s)

What it is: Your most recent pay stubs — typically the last 30 days’ worth — plus W-2 forms from your employer for the past two years. If you receive bonuses, commissions, or overtime, those will show up here too.

Why lenders need it: Lenders need to verify that you’re earning what you say you’re earning, and that your income is stable. Pay stubs give them a real-time snapshot of your current earnings, while W-2s confirm your income history over time. Together, they help the lender calculate your gross monthly income — one of the most important numbers in your mortgage application.

Here’s where most people get stuck: Many buyers assume their current salary is what matters most. But lenders look at your average income over time, especially if your earnings fluctuate. If you earned $85,000 last year but switched to a commission-based role this year, that change could raise flags — even if you’re making more money now.

Document #2: Federal Tax Returns (Last 2 Years)

What it is: Complete federal tax returns — including all schedules — for the past two tax years. If you file jointly with a spouse, lenders will want both of your returns. Most lenders require signed copies or IRS Form 4506-C, which authorizes them to request your tax transcripts directly from the Internal Revenue Service (IRS).

Why lenders need it: Tax returns are especially critical for self-employed borrowers, freelancers, gig workers, and anyone whose income isn’t a straightforward salary. They tell lenders what you actually earned after deductions — not just what your invoices say. For salaried employees, tax returns serve as a cross-check against the W-2s and pay stubs you’ve already provided.

This trips up a lot of buyers — especially business owners. If you write off a large portion of your income as business expenses, your taxable income on paper may be much lower than what you actually bring home. Lenders use your adjusted gross income (AGI) or net profit as shown on your returns, which could reduce the loan amount you qualify for.

Document #3: Bank Statements (2–3 Months)

What it is: Full statements from all of your bank accounts — checking, savings, money market, and sometimes investment accounts — for the past 2 to 3 months. Lenders want to see the complete statement, not just a summary or a screenshot.

Why lenders need it: Your bank statements serve two major purposes. First, they verify that you actually have the funds to cover your down payment and closing costs. Second, they help lenders assess whether you’ll have any reserves left over after closing — since lenders prefer borrowers who don’t drain their entire savings to buy a home.

Ever wondered why lenders care so much about your bank balance? It’s not just about whether you have enough for the down payment. They’re looking at the overall picture of your financial health — how much you save, how much you spend, and whether your deposits match your stated income.

If you’re keeping close tabs on your spending, apps like YNAB (You Need a Budget) or Mint can help you track and organize your financial picture before you apply — giving you a cleaner bank statement history to show lenders.

Document #4: Credit History & Credit Authorization

What it is: You won’t need to hand over a printed credit report — instead, you’ll sign a credit authorization form giving the lender permission to pull your credit report directly from the three major bureaus: Equifax, Experian, and TransUnion. The lender will use your FICO score and credit history as a key part of their decision.

Why lenders need it: Your credit report shows how reliably you’ve repaid debts in the past. It includes payment history, outstanding balances, length of credit history, types of credit, and any negative marks like late payments, collections, or bankruptcies. This information feeds into your credit score, which directly affects your mortgage interest rate.

According to the Consumer Financial Protection Bureau (CFPB), even a small difference in credit score can significantly impact your interest rate over the life of a 30-year loan. A score of 760 vs. 680 could mean a difference of half a percentage point or more — which adds up to tens of thousands of dollars over time.

Using a credit monitoring service like Experian CreditWorks can alert you to changes in your credit report in real time, helping you catch problems before lenders do. For more, see our guide on the average credit score in the U.S.

Document #5: Employment Verification

What it is: Official confirmation that you are employed and in your current position. This can take several forms: a Verification of Employment (VOE) letter from your employer on company letterhead, a recent offer letter if you’ve just started a new job, or contact information for your employer’s HR department so the lender can verify directly.

Why lenders need it: Lenders don’t just want to know that you were employed when you applied — they want assurance that your income is likely to continue. Employment verification helps confirm your job title, tenure, and whether you’re full-time, part-time, or contract. It’s one more layer of confirmation that the income on your pay stubs is real and ongoing.

I’ve seen this delay approvals more than anything else: A job change during underwriting. If you switch employers after submitting your application — even to a better-paying job — your lender may need to restart parts of the verification process. In some cases, it can cause your loan to fall through entirely.

Document #6: Government-Issued Identification

What it is: A valid, current government-issued photo ID such as a U.S. driver’s license, state ID, or passport. You’ll also need to provide your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) if applicable.

Why lenders need it: This one is required by federal law. Under the USA PATRIOT Act, financial institutions must verify the identity of all customers applying for loans. Lenders use your ID to confirm that you are who you say you are and to run required background checks. Your SSN is also used to pull your credit report and locate your tax records.

Document #7: Debt & Liability Records

What it is: A complete picture of your existing financial obligations. This includes monthly payments for credit cards, student loans, car loans, personal loans, child support, alimony, and any other recurring debt. Most of this will show up on your credit report, but lenders may ask you to provide monthly statements for specific accounts.

Why lenders need it: Your debt-to-income (DTI) ratio is one of the most important numbers in your mortgage application. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Most conventional lenders prefer a DTI below 43%, and many prefer 36% or lower. The lower your DTI, the more borrowing power you have.

The Consumer Financial Protection Bureau explains that your debt-to-income ratio is one of the most critical metrics lenders use to assess your ability to manage monthly payments and repay debts.

At-a-Glance Comparison: All 7 Documents

Here’s your quick-reference guide to every document you’ll need:

| Document | Why It Matters | Common Mistake | Pro Tip |

|---|---|---|---|

| 💼 Pay Stubs (Last 30 days) | Proves current, stable income to lender | Using stubs older than 30 days | Get the most recent 2–4 pay stubs |

| 🧾 Tax Returns (2 Years) | Shows consistent income, especially for self-employed | Missing schedules or signatures | Provide full returns, not just the 1040 summary |

| 🏦 Bank Statements (2–3 Months) | Verifies funds for down payment & closing | Unexplained large deposits flagged | Avoid cash deposits 60–90 days before applying |

| 📊 Credit Authorization | Allows lender to pull your credit report | Disputing errors after applying (too late) | Check credit 3–6 months before applying |

| ✅ Employment Verification | Confirms job stability and title | Job change during underwriting process | Never switch jobs mid-application |

| 🪪 Government-Issued ID | Identity verification (PATRIOT Act compliance) | Expired ID or name mismatch | Ensure name matches all documents exactly |

| 📉 Debt & Liability Records | Calculates your DTI ratio | Forgetting car loans or student loans | List every monthly obligation honestly |

How to Prepare Your Mortgage Documents Without Stress

Gathering these documents doesn’t have to feel like a scavenger hunt. Here’s a step-by-step approach that takes the chaos out of the process:

🧾 Special Situations: Self-Employed Borrowers

If you’re self-employed — whether as a freelancer, independent contractor, business owner, or gig worker — the mortgage process requires a few extra steps. Lenders need more documentation to verify your income because it doesn’t come from a traditional employer.

In addition to the 7 standard documents, self-employed borrowers typically need:

A friend of mine who runs a small landscaping company in Ohio went through this exact process last year. He’d been in business for six years, was profitable, and had great credit — but the mortgage process still took nearly two months because his income looked inconsistent on paper due to the seasonal nature of his work. His CPA wrote a detailed explanation letter, and he ultimately got approved. The lesson? Plan ahead and have professional support in your corner.

For self-employed borrowers, working with a mortgage broker who specializes in non-traditional income situations can be incredibly valuable. They often have access to bank statement loans, which qualify you based on 12–24 months of bank deposits rather than tax returns. Also see our guide on refinancing a mortgage for more borrowing strategies.

Frequently Asked Questions

Final Thoughts: You’re More Prepared Than You Think

Once you have these 7 documents ready, you’re already ahead of most buyers. The mortgage process can feel overwhelming at first — there’s a lot of paperwork, a lot of terminology, and a lot at stake. But the truth is, once you understand what lenders are looking for and why, it starts to feel much more manageable.

The key is preparation. Start early. Get organized. Be honest about your financial picture — lenders will find out anyway, and coming in prepared shows them you’re a responsible borrower. And don’t be afraid to ask questions. A good loan officer will walk you through the process and tell you exactly what they need.

Buying a home is one of the biggest financial decisions of your life. The paperwork is just the beginning — and it’s the part you can absolutely control. Get these documents in order, and you’ll walk into that lender’s office with confidence.

Additional Resources and Tools Worth Knowing

Here are a few tools and resources that can make the mortgage preparation process smoother:

|

One of the most comprehensive free resources for U.S. homebuyers — walks through every stage of the process.

|

List of HUD-approved housing counselors who provide free or low-cost guidance on the homebuying process.

|

|

The only federally authorized source for free credit reports from all three major bureaus. Check before any lender does.

|

The official guide used by FHA-approved lenders nationwide — covers all FHA loan documentation standards.

|

| What is a Personal Loan? | How to Qualify for a Loan | Average Credit Score in the U.S. |

| Refinancing a Mortgage | How Loan Interest Works |

Disclosure: This article is for informational purposes only and does not constitute financial, legal, or lending advice. Always consult a licensed mortgage professional before making decisions about your home loan.