Table of Contents

This guide was written by a personal finance specialist with over 12 years of experience in residential mortgage advising. All calculations, scenarios, and recommendations are based on current industry data from the Federal Reserve, Consumer Financial Protection Bureau (CFPB), and Freddie Mac’s Primary Mortgage Market Survey. We update this guide regularly to reflect current rate environments. External sources referenced: Federal Reserve (federalreserve.gov) | CFPB (consumerfinance.gov) | Freddie Mac (freddiemac.com) | HUD (hud.gov)

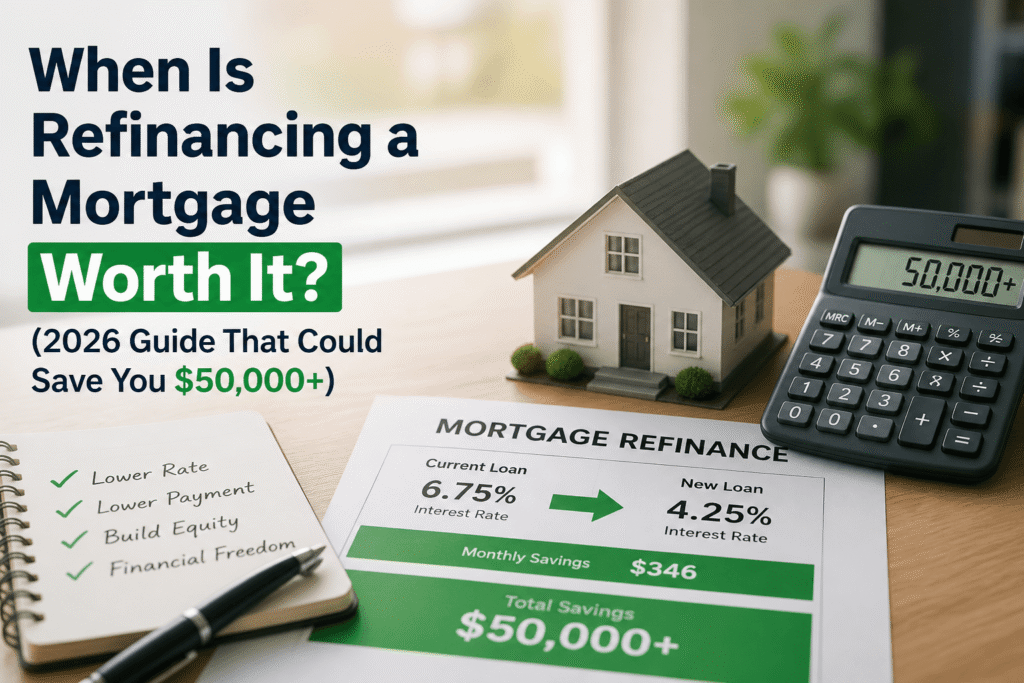

Refinancing your mortgage is worth it when you can lower your interest rate by at least 0.75%–1% or more, your new monthly savings will cover the closing costs within 2–3 years (the break-even point), and you plan to stay in your home beyond that point. If you’re moving soon, just reset your loan, or won’t recoup closing costs in time, refinancing is likely not worth the hassle — and could actually cost you more money in the long run.

What Does Refinancing Actually Mean?

Let’s start simple, because a lot of people have a rough sense of what refinancing is — but not the full picture.

When you refinance your mortgage, you’re essentially replacing your existing home loan with a brand-new one — ideally with better terms. The new lender pays off your old mortgage, and you start making payments on the new loan.

Think of it like trading in your old car loan for a new one with a lower interest rate. Same house, new deal.

Here’s what can change when you refinance:

One thing people often miss: refinancing isn’t free. You’ll pay closing costs — typically 2%–5% of your loan amount — just like you did when you originally bought the home. That’s why the math matters so much.

According to the Consumer Financial Protection Bureau, refinancing can save money but requires careful evaluation of your financial situation and goals before proceeding.

When Is Refinancing Worth It?

This is where most guides give you a vague “it depends” and leave you hanging. Not this one. Here are the specific situations where refinancing actually makes financial sense:

1. Your Interest Rate Will Drop by 0.75% or More

This is the golden rule of refinancing. A rate drop of even 1% on a $300,000 loan can save you around $180–$200 per month — and well over $50,000 across a 30-year loan term.

Let’s run the numbers quickly:

Even after paying $6,000–$9,000 in closing costs, the numbers make a strong case here. But we’ll talk about the break-even point in detail shortly.

2. You Want a Shorter Loan Term

Here’s something a lot of homeowners don’t realize: refinancing from a 30-year to a 15-year mortgage can dramatically reduce the total interest you pay — even if your monthly payment goes up a bit.

The interest savings on a 15-year loan can be staggering. On a $250,000 loan at 6.5%, you’d pay roughly $285,000 in interest over 30 years. On a 15-year loan at 6.0%, that drops to about $130,000. That’s $155,000 in savings. That’s a college education, a retirement cushion, or a vacation home.

This works best if your income has grown since you first bought the home and you can handle the higher payment comfortably.

3. You’re Switching From an ARM to a Fixed Rate

Adjustable-rate mortgages start low and then fluctuate based on market conditions. If your ARM is about to reset — or you’re worried about rates climbing — locking into a fixed rate gives you stability and peace of mind.

The Federal Reserve’s rate decisions directly affect ARM rates, which is why many homeowners prefer the predictability of a fixed mortgage.

4. You Can Remove Private Mortgage Insurance (PMI)

If you put less than 20% down when you bought your home and your home’s value has since increased, you might now have 20%+ equity. Refinancing can eliminate the PMI you’re currently paying — which often runs $100–$250 per month.

That’s a meaningful saving every month, for the life of the loan — or at least until you would have had 20% equity otherwise.

5. You Want to Do a Cash-Out Refinance

A cash-out refi lets you borrow more than you currently owe and pocket the difference. For example, if your home is worth $450,000 and you owe $250,000, you might refinance for $320,000 and take out $70,000 in cash.

This makes sense when:

But be careful — you’re putting your home on the line. This isn’t money you should spend on vacations or depreciating assets.

When Refinancing Is NOT Worth It

Here’s the flip side — and this part is just as important. Plenty of homeowners refinance at exactly the wrong time and end up worse off. Let’s talk about the red flags.

A tiny rate reduction sounds great, but after you factor in 2%–5% in closing costs, you might need 8–10+ years just to break even. If you’re not planning to stay in the home that long, you’re losing money.

This is one of the most common refinancing mistakes. You refi, pay $8,000 in closing costs, save $200/month… and then sell the house 18 months later. You’ve lost money. Period. Always match your refinancing timeline to your actual life plans.

Mortgages are front-loaded with interest. In the early years, most of your payment goes toward interest. By year 20+, you’re mostly paying down principal. If you refinance into a new 30-year loan at that point, you restart the interest clock — and end up paying dramatically more total interest, even if your monthly payment goes down. This is where people get tricked by a lower monthly payment that actually costs them more over time.

If your credit score has decreased since your original mortgage, you may not qualify for a competitive rate. According to Freddie Mac’s research, borrowers with scores below 620 face significantly higher rates or may not qualify at all. In that case, it’s worth improving your credit first. Learn how to raise your credit score fast.

If you’re underwater on your mortgage (you owe more than the home is worth), most lenders won’t refinance you unless you qualify for a specialized program. Check your home’s current value using tools like Zillow or your county assessor’s website before assuming you’re eligible.

Some lenders offer “no-closing-cost” refinancing — but they often roll those fees into a higher interest rate or the loan balance. You’re still paying them; you just don’t see them upfront. Always read the fine print.

The Break-Even Rule: The Only Number That Really Matters

This is genuinely the most important concept in this entire article. If you only take one thing away from this guide, let it be this:

Simple, right? Here’s why people mess this up: they see the lower monthly payment and get excited — without doing the math on how long it takes to actually recoup what they paid upfront.

The break-even point is your decision line. If you’re staying in the home longer than that number, refinance. If not, don’t.

You can calculate your break-even point using tools from the CFPB’s mortgage refinance calculator, which allows you to compare offers side by side based on your actual loan numbers.

One more thing: don’t forget taxes. If you itemize deductions, mortgage interest is deductible. A lower interest payment means a slightly smaller deduction, which can affect your real after-tax savings. Talk to a tax advisor if this applies to you.

Real-Life Scenarios: When Refinancing Worked — and When It Didn’t

Sometimes the best way to understand financial decisions is to see them in action. Here are three realistic scenarios to show how this plays out:

How to Decide If Refinancing Makes Sense (Step-by-Step)

Ready to figure out if refinancing is right for you? Here’s exactly what to do, in order:

Refinancing Comparison Table: Is It Worth It?

Here’s a quick visual summary to help you think through your specific situation:

| Situation | Worth It? | Why |

|---|---|---|

| Rate drops by 1%+, staying 5+ years |

Yes — Strong

|

High savings, ample time to break even |

| Rate drops by 0.5%, staying 3+ years |

Maybe — Do Math

|

Borderline; break-even could be 4+ years |

| Rate drops 0.25%, moving in 2 years |

No

|

Won’t recoup closing costs in time |

| 30-yr to 15-yr term, income is stable |

Yes — Great

|

Massive interest savings over time |

| ARM to Fixed rate, rates rising |

Yes

|

Stability + potential savings |

| Cash-out for home renovation |

Depends

|

Works if ROI > refinance cost |

| Cash-out for vacation/car |

No

|

Depreciating assets, real risk |

| Credit dropped since original loan |

Probably Not

|

Rate may be worse; improve credit first |

| 20+ years into 30-yr mortgage |

Be Careful

|

Restarting interest clock can cost more |

| Remove PMI (now have 20%+ equity) |

Yes (if rate is good)

|

Eliminate $100–$250/mo PMI payment |

What Credit Score Do You Need to Refinance?

Your credit score is one of the biggest factors lenders look at. Here’s a general breakdown:

| Credit Score Range | Refinance Eligibility | Expected Rate Impact |

|---|---|---|

| 760–850 (Excellent) | Qualifies for best rates | Lowest available rates |

| 700–759 (Good) | Strong eligibility | Slightly higher than top tier |

| 660–699 (Fair) | Eligible with most lenders | Noticeably higher rates |

| 620–659 (Marginal) | Limited options, higher rates | May add 0.5%–1%+ to your rate |

| Below 620 | Difficult to qualify | May need FHA or special programs |

Before applying, it’s worth checking your credit score and report. You can get your free annual credit report from AnnualCreditReport.com — the only federally authorized site for free credit reports. Many banks also offer free FICO score tracking through their apps.

If your score needs a boost, here’s what moves the needle most:

Understanding Refinancing Costs (The Full Picture)

Here’s something that trips a lot of people up: they focus on the new interest rate and forget about the closing costs. Let’s break down what you’ll typically pay:

| Cost Item | Typical Range | Notes |

|---|---|---|

| Origination fee | 0.5%–1% of loan | Lender’s processing fee; sometimes negotiable |

| Appraisal fee | $300–$700 | Required to verify home’s current value |

| Title search & insurance | $500–$1,500 | Verifies ownership history |

| Recording fees | $25–$250 | Government fee to record the new deed |

| Credit report fee | $25–$50 | Lender pulls your credit |

| Prepaid interest | Varies | Interest from closing to first payment |

| Escrow setup | $300–$600 | Initial funding of tax/insurance escrow |

| Attorney fees (if req’d) | $500–$1,000 | Required in some states |

| TOTAL CLOSING COSTS | 2%–5% of loan | $6,000–$15,000 on a $300K loan |

Total closing costs: typically 2%–5% of your loan amount. On a $300,000 loan, that’s $6,000–$15,000. Always get the full Loan Estimate before committing — and ask every lender what’s negotiable. The U.S. Department of Housing and Urban Development (HUD) provides resources to help you understand all the costs involved in refinancing and your rights as a borrower.

How Refinancing Affects Your Credit Score

Short answer: it causes a temporary dip, but it’s not a disaster.

Here’s what happens when you apply to refinance:

Most people see their score recover and often improve within 12 months as they make consistent on-time payments on the new loan. Unless you’re about to apply for another major loan (car, business), a refinance’s credit impact is a minor concern. Learn more about how late payments affect credit and what you can do to protect your score.

Refinancing FAQs: The Questions Everyone Googles

Final Thoughts: Make the Math Work for You

Here’s the bottom line: refinancing your mortgage can be one of the most financially impactful decisions you’ll ever make — or a costly mistake if you do it at the wrong time.

The good news? The math is actually pretty simple. Know your break-even point. Know your timeline. Shop multiple lenders. And make sure your credit score is working in your favor before you apply.

Don’t let a lower monthly payment dazzle you before you’ve done the full calculation. And don’t let fear of complexity keep you from saving tens of thousands of dollars if the numbers genuinely line up.

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates and terms vary by lender, borrower profile, and market conditions. Always consult a licensed mortgage professional or financial advisor before making refinancing decisions.