Quick Summary

|

|

||||

|

|

||||

|

|

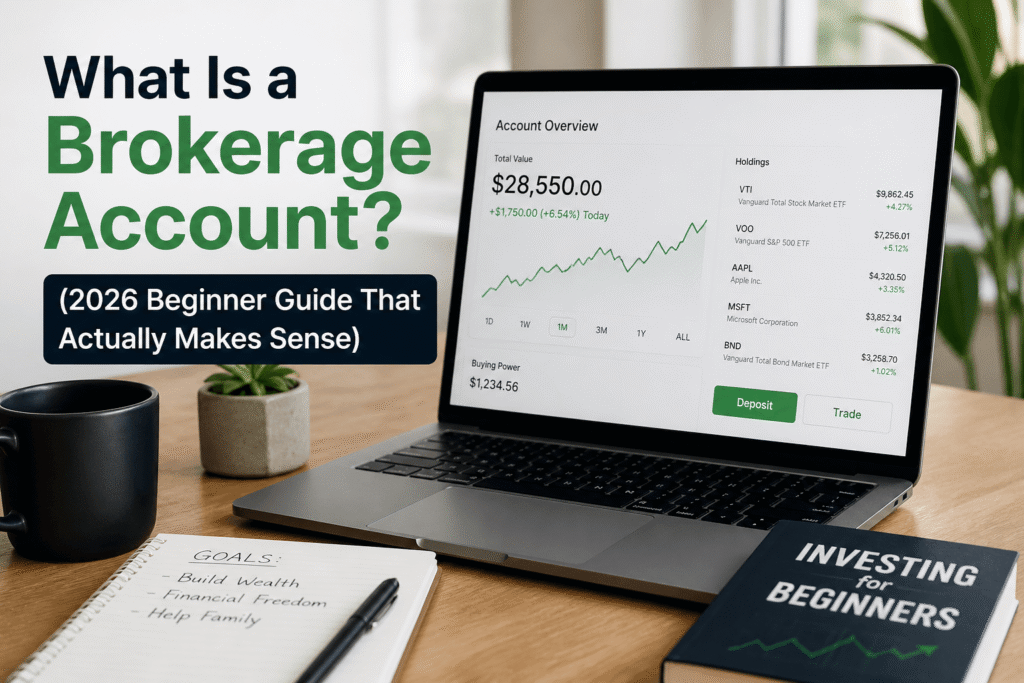

What Is a Brokerage Account?

Think of a brokerage account like a wallet — but instead of holding cash, it holds investments. You deposit money into it, and then use that money to buy assets that (hopefully) grow over time.

A broker is essentially the middleman between you and the stock market. In the old days, you’d call a broker on the phone to place a trade. Today, platforms like Fidelity, Charles Schwab, and Robinhood let you do it all yourself from an app.

Here’s the thing: you don’t need to be a finance expert to open one. You just need a government-issued ID, a Social Security number, and a bank account to fund it.

“A brokerage account is the front door to investing. Once you have one, the entire market is accessible to you.”

How a Brokerage Account Actually Works

Let’s walk through it step by step, because it’s honestly simpler than most people think.

|

1

|

Deposit MoneyYou transfer cash from your bank account into your brokerage account. This is called funding your account. It usually takes 1–3 business days to settle, though some platforms offer instant buying power. |

|

2

|

Buy InvestmentsOnce your money is in, you can search for stocks, ETFs, mutual funds, or other assets and place a buy order. You choose how much to invest, hit confirm, and boom — you’re an investor. |

|

3

|

Watch It Grow (or Fluctuate)Your investments will move up and down with the market. That’s normal. The goal is for the overall trend to be upward over time. You can track everything in your account dashboard. |

|

4

|

Sell When ReadyWhen you’re ready to cash out — whether that’s in 6 months or 20 years — you sell your investments. The money goes back into your brokerage account as cash, and you can withdraw it to your bank. Important: Selling at a profit triggers a taxable event. We’ll cover taxes in detail later. |

Types of Brokerage Accounts

🧑 Individual Brokerage Account

The most common type. You own it solo, and all the gains, losses, and tax obligations are yours. Perfect for solo investors just getting started.

👫 Joint Brokerage Account

Shared between two people — usually married couples or business partners. Both parties have equal rights to the assets. Useful if you’re investing alongside a spouse toward a shared goal like buying a home.

👶 Custodial Account (UTMA/UGMA)

An adult opens and manages this on behalf of a minor. When the child turns 18 (or 21, depending on the state), the account transfers to them. Great for parents who want to start building wealth for their kids early.

🤖 Managed / Robo-Advisor Accounts

If you don’t want to pick investments yourself, robo-advisors like Betterment or Wealthfront do it for you. They build a diversified portfolio based on your goals and risk tolerance — automatically. You pay a small annual fee (usually around 0.25%), but it’s hands-off investing at its best.

Brokerage Account vs. Retirement Account: What’s the Difference?

This is one of the most common questions beginners ask — and honestly, it trips a lot of people up. Here’s a simple breakdown:

| Feature | Brokerage Account | IRA | 401(k) |

|---|---|---|---|

| Contribution Limit | No limit | $7,000/yr (2026) | $23,500/yr (2026) |

| Tax Treatment | Taxed on gains/dividends | Tax-deferred or tax-free (Roth) | Pre-tax contributions |

| Withdrawal Rules | Anytime, no penalty | Penalty before 59½ | Penalty before 59½ |

| Employer Match | No | No | Often yes (free money!) |

| Investment Choices | Stocks, ETFs, bonds, options, etc. | Stocks, ETFs, mutual funds | Limited to plan options |

| Best For | Flexible investing, short/long-term | Retirement tax savings | Employer-sponsored retirement |

💡 The smart move for most people? Use all three. Max out your 401(k) match first (free money!), then contribute to an IRA, and use a brokerage account for anything beyond that.

What Can You Actually Invest In?

A brokerage account opens the door to almost every major type of investment. Here’s what you’ll commonly find:

| 📈 |

StocksBuying a share of stock means you own a tiny slice of a company. If Apple does well, your shares do well. High potential reward, but also higher risk. |

| 🧺 |

ETFs (Exchange-Traded Funds)ETFs are like a pre-made basket of stocks. One popular example: Vanguard’s VTI gives you exposure to the entire U.S. stock market in a single purchase. They’re diversified, low-cost, and beginner-friendly — which is why most financial advisors love them. |

| 💼 |

Mutual FundsSimilar to ETFs but actively managed by a fund manager. They typically come with higher fees (called expense ratios). Index mutual funds are a lower-cost alternative. |

| 🏛️ |

BondsBonds are loans you give to governments or corporations in exchange for regular interest payments. They’re generally safer than stocks but offer lower returns. Good for balancing a portfolio. |

| ⚠️ |

Options (Advanced — Proceed with Caution)Options let you speculate on whether a stock will go up or down by a certain date. They’re complex and risky. We’d recommend skipping these until you have at least a year of investing experience under your belt. |

| 🏢 |

REITs, Crypto, and MoreMany brokerages also offer Real Estate Investment Trusts (REITs) and some even offer crypto trading. The world of investing is wide — you don’t need to explore it all at once. |

Real-Life Example: Meet Sarah

Sarah is 27, works as a graphic designer, and has $1,000 sitting in her savings account earning 0.01% interest. She opens a brokerage account with Fidelity and transfers $1,000.

She decides to invest in a simple S&P 500 index ETF (like SPY). Historically, the S&P 500 has returned an average of about 10% per year.

|

$1,000

Starting Balance

|

→ |

$2,594

After 10 Years (~10%/yr)

|

Here’s the emotional reality though: In year three, the market drops 20%. Sarah panics. She almost sells. Instead, she reminds herself she’s investing for the long haul — and holds. A year later, the market recovers and she’s up again.

That moment of almost panic-selling but choosing to stay invested? That’s the most important investing decision most beginners ever make.

Pros and Cons of a Brokerage Account

✔ Pros+ No contribution limits — invest as much as you want + Withdraw your money anytime without penalty + Access to a huge range of investments + Flexible — can be used for short-term or long-term goals + Fractional shares available on many platforms (invest $10 in Amazon, not $3,000) |

✘ Cons− No upfront tax benefits (unlike 401k or IRA) − Gains and dividends are taxable in the year they occur − Your money is at market risk — no FDIC protection on investments − More decisions = more chances to make emotional mistakes |

Common Beginner Mistakes (And How to Avoid Them)

Honestly, this is where most beginners get stuck. Not because investing is hard — but because emotion gets in the way. Here are the biggest mistakes to watch out for:

Mistake #1: Investing Without a Plan

Randomly buying stocks because you heard about them on Reddit is not a strategy. Before you invest a single dollar, know your goal. Is this for retirement in 30 years? A house in 5 years? The answer shapes everything.

Mistake #2: Panic Selling

The market drops. You feel sick. You sell. Then the market recovers and you’ve locked in a loss. This is the single most common — and costly — beginner mistake. Time in the market beats timing the market.

Mistake #3: Ignoring Fees

A 1% annual fee sounds tiny. Over 30 years, on a $100,000 portfolio, it can cost you over $94,000 in lost growth. Always check expense ratios on ETFs and mutual funds. Index funds often charge as low as 0.03%.

Mistake #4: Overtrading

Buying and selling frequently racks up taxes and fees — and usually leads to worse returns than simply holding. Studies consistently show that passive investors outperform active traders over the long run.

Mistake #5: Putting All Your Eggs in One Basket

Investing your entire portfolio in one stock (even a great company) is a gamble. Diversify across multiple companies, sectors, or just use a broad index fund that does it for you automatically.

Mistake #6: Waiting for the “Perfect” Time to Invest

There is no perfect time. People have been saying “wait until the market corrects” for decades, and most of them have missed enormous growth. The best time to start was yesterday. The second best time is today.

How to Choose the Best Brokerage Account for Beginners

Not all brokerages are created equal. Here’s what to look for — and a few options worth considering:

What to Look For

|

💲 $0 Commission Trades

Standard now, but double-check. Most major platforms offer this. |

🔓 No Account Minimum

You shouldn’t need $1,000 to start. Many platforms let you begin with $1. |

|

🍕 Fractional Shares

Lets you buy partial shares of expensive stocks like Amazon or Tesla. |

📚 Educational Resources

Especially important for beginners. Look for guides, videos, and research tools. |

|

📞 Customer Support

24/7 phone or chat support matters when something feels confusing. |

📱 Mobile App Quality

If you’ll mostly invest on your phone, make sure the app is smooth and reliable. |

Top Brokerage Platforms at a Glance

| Platform | Best For | Stock Trades | Min. Balance | Standout Feature |

|---|---|---|---|---|

| Fidelity | All-around beginners | $0 | $0 | Research tools + 24/7 support |

| Charles Schwab | Long-term investors | $0 | $0 | Fractional shares, great education |

| Robinhood | Mobile-first beginners | $0 | $0 | Simple app, crypto access |

| TD Ameritrade | Active traders | $0 | $0 | thinkorswim platform |

| Betterment | Hands-off investors | N/A (robo) | $0 (0.25%/yr fee) | Auto-rebalancing, tax-loss harvesting |

For completely hands-off investing, robo-advisors like Betterment or Wealthfront are excellent. They automatically build and rebalance a diversified portfolio for you. Perfect if you’d rather set it and forget it.

| 📱 |

Want a deeper comparison? Check out our guide on Best Investing Apps for Beginners — we reviewed every major platform head-to-head. |

Are Brokerage Accounts Safe?

Short answer: yes — but it’s worth understanding what’s protected and what isn’t.

|

🛡️

SIPC InsuranceMost brokerage accounts are protected by the SIPC. If your brokerage goes bankrupt, SIPC covers up to $500,000 in securities and $250,000 in cash. This protects you from the brokerage failing — not from market losses. |

🔐

Platform SecurityReputable brokerages use two-factor authentication, encryption, and fraud monitoring. Always enable 2FA on your account and use a strong, unique password. |

📉

Market Risk Is RealHere’s what SIPC does NOT protect against: the market going down. If you invest $10,000 and the market drops 30%, your portfolio is worth $7,000. Markets recover and grow over time — but short-term losses are real. |

Your brokerage is safe. Your investments carry risk. Both things can be true at once.

Taxes on Brokerage Accounts (Explained Simply)

Taxes are the part nobody wants to talk about — but ignoring them is how you get surprised in April. Here’s the simplified version:

💰 Capital Gains Tax

|

⚡ Short-Term Capital Gains

If you sell an investment you’ve held for less than one year, the profit is taxed as ordinary income — the same rate as your salary. This can be 22%, 24%, or higher depending on your bracket. |

🌿 Long-Term Capital Gains

Hold an investment for more than one year before selling, and you pay the lower long-term capital gains rate — typically 0%, 15%, or 20% depending on your income. This is a huge incentive to hold longer. |

📬 Dividend Tax

If a stock pays dividends (regular cash payments to shareholders), those are also taxable. Qualified dividends are taxed at the lower long-term rate; ordinary dividends at your regular income rate.

🌾 Tax-Loss Harvesting

If some investments are down, you can sell them at a loss to offset gains elsewhere — reducing your overall tax bill. This is a legitimate strategy used by smart investors. Some robo-advisors do this automatically.

For more detailed tax guidance, the IRS Publication 550 is the official source — though speaking with a CPA is always worth it for personalized advice.

| 🧾 |

Learn more: Federal Income Tax Brackets Explained |

How to Open a Brokerage Account (Step-by-Step)

Good news: this takes about 15 minutes. Here’s exactly what to do:

|

1

|

Choose your brokerage platform. Beginners often do well with Fidelity or Charles Schwab for their education resources, or Robinhood if you want something super simple. |

|

2

|

Go to the platform’s website or download their app. Click “Open an Account” or “Get Started.” |

|

3

|

Fill out the application. You’ll need: full legal name, Social Security Number, date of birth, address, employment status, and estimated annual income & net worth. |

|

4

|

Choose your account type. For most beginners, a standard “Individual Brokerage Account” (also called a taxable account) is the right choice. |

|

5

|

Fund your account by linking your bank account and transferring money. Start small if you’re nervous — even $50 is enough to begin learning. |

|

6

|

Pick your first investment. If you’re unsure where to start, a broad market index ETF (like VTI or SPY) is a great first choice. It gives you diversified exposure to hundreds of companies at once. |

|

7

|

Set up automatic contributions if possible. Investing a fixed amount monthly — regardless of market conditions — is called dollar-cost averaging, and it’s one of the smartest long-term strategies. |

|

8

|

Monitor periodically — not obsessively. Checking your portfolio once a month is plenty. Daily checking leads to emotional decisions. |

Frequently Asked Questions

Final Thoughts: Just Start

Here’s the honest truth: the hardest part of investing isn’t picking the right stock or understanding the tax code. It’s starting.

Most people spend years feeling like they need to know more before they’re “ready.” But the greatest risk in investing isn’t that the market might go down — it’s that you stay on the sidelines while inflation quietly erodes the value of your savings.

A brokerage account gives you access to the same wealth-building tools that wealthy families have used for generations. The barrier to entry is now $0, and the process takes 15 minutes.

You don’t need to be rich or a finance expert to start. You just need to start. Open an account, invest in something simple, and give it time. Future you will be very grateful.

Keep Learning

For more beginner-friendly investing content, check out resources like Investopedia’s Investing Basics or the SEC’s Investor.gov — a free, official resource for learning how markets work.

This content is for informational purposes only and does not constitute financial advice. Always consult a qualified financial advisor before making investment decisions.