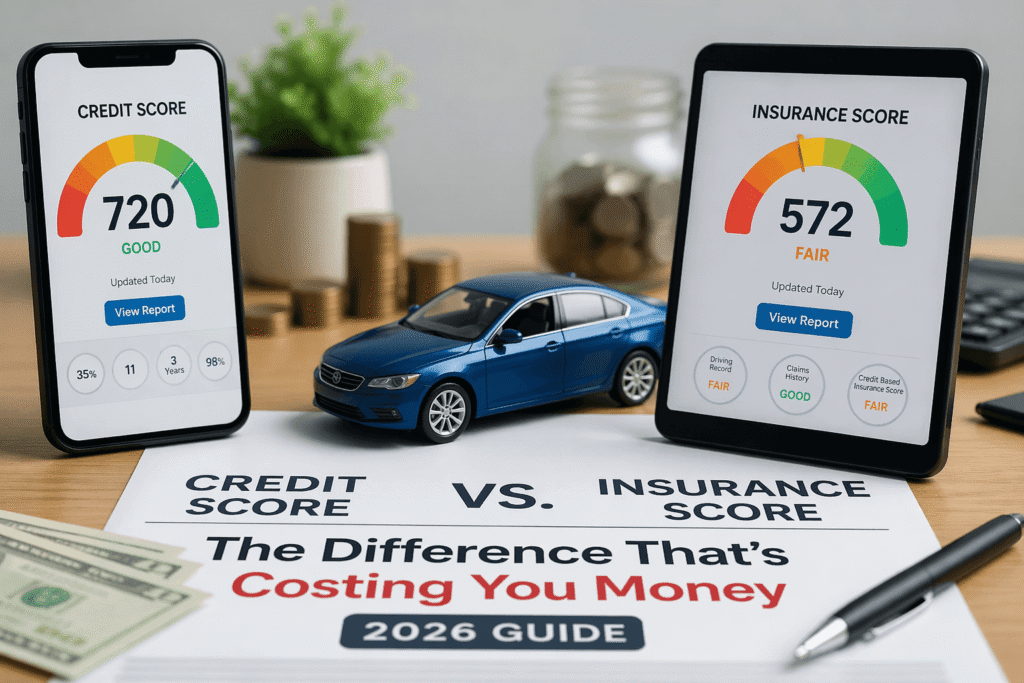

QUICK ANSWER: A credit score measures your ability to repay debt and is used by lenders. A credit-based insurance score predicts how likely you are to file an insurance claim and is used by insurers. Both pull from the same credit data — but they calculate it differently, mean different things, and affect very different parts of your financial life. Here’s what you need to know.

Quick Summary

- ✓Credit score = used by banks and lenders to decide if you can borrow money

- ✓Insurance score = used by insurers to predict whether you’ll file a claim

- ✓Both scores use similar credit data, but weigh factors very differently

- ✓A great credit score does NOT guarantee a great insurance score

- ✓Your insurance score directly impacts your auto and home insurance premiums

- ✓Improving your credit habits helps both — but the effect isn’t equal

- ✓Several states restrict or ban the use of insurance scores entirely

Wait — There Are Two Different Scores?

Most people spend years carefully building their credit score — paying bills on time, keeping balances low, avoiding unnecessary hard inquiries — all with the goal of getting better loan rates and credit card offers. That makes total sense.

But here’s what most financial guides don’t tell you: there’s a completely separate score running in the background that can quietly raise your insurance premiums by hundreds of dollars a year. And the frustrating part? You’ve probably never even heard of it.

It’s called a credit-based insurance score. And while it sounds like your credit score, it works differently, means something different, and is used by a completely different industry.

Let’s break both of these down — simply and clearly — so you know exactly what you’re dealing with.

What Is a Credit Score?

Think of your credit score as your financial reputation. It’s a three-digit number — typically ranging from 300 to 850 — that tells lenders how reliable you are when it comes to borrowing and repaying money.

The two most common models are FICO and VantageScore. Most lenders use FICO, but both pull from data reported by the three major credit bureaus: Equifax, Experian, and TransUnion.

What Goes Into Your Credit Score?

FICO breaks it down like this:

35%

Do you pay on time? This is the biggest factor.

30%

How much of your available credit are you using?

15%

How long have your accounts been open?

10%

Do you have a variety of account types (cards, loans, mortgage)?

10%

Have you recently applied for new accounts?

Here’s a quick breakdown of what different score ranges mean:

| Score Range | Rating | What It Means |

|---|---|---|

| 800–850 | Exceptional | Best rates, easiest approvals |

| 740–799 | Very Good | Near-best rates |

| 670–739 | Good | Average approval odds |

| 580–669 | Fair | Subprime territory |

| 300–579 | Poor | Difficult to get credit |

Your credit score is used any time you apply for a credit card, mortgage, auto loan, or even sometimes when renting an apartment. The higher the score, the better the terms you’ll generally get.

What it does NOT do, though? Predict how often you’ll file an insurance claim. And that’s where the insurance world decided it needed its own tool.

What Is a Credit-Based Insurance Score?

A credit-based insurance score is a special number — usually between 200 and 997 — that insurance companies use to predict how likely you are to file a claim. It’s created by companies like FICO, LexisNexis, and TransUnion, and it’s specifically designed for the insurance industry.

Here’s the key thing to understand: it’s not your credit score. It looks similar. It uses similar data. But it’s calculated differently and weighted differently, because it’s answering a different question.

What Factors Go Into an Insurance Score?

While the exact formulas are proprietary (companies like FICO don’t publish them in full), research and regulatory filings give us a good picture:

- Payment history — Late payments signal financial stress, which correlates with more claims

- Outstanding debt — High balances relative to limits are a red flag

- Length of credit history — Longer histories generally mean more stability

- Types of credit used — Mix of account types matters

- New credit applications — Lots of recent inquiries can indicate financial instability

Notice how similar that looks to your credit score factors? Right. That’s because they use overlapping data — but weight the factors very differently based on what they’re trying to predict.

Real Example: Imagine two neighbors, Sarah and James. Both have a 720 credit score. Sarah has a long credit history with low utilization and zero late payments. James has a shorter history, high utilization, and a couple of missed payments he later caught up on. Their credit scores might look identical on the surface — but their insurance scores could be meaningfully different, leading to different premiums.

Credit Score vs. Insurance Score: Side-by-Side Comparison

Here’s the comparison table you’ve been waiting for. Bookmark this — it’s the clearest breakdown you’ll find anywhere:

| Factor | Credit Score | Credit-Based Insurance Score |

|---|---|---|

| Primary Purpose | Measures ability to repay debt | Predicts likelihood of filing a claim |

| Who Uses It | Banks, lenders, credit card companies | Auto and home insurance companies |

| What It Affects | Loan approvals, interest rates | Your monthly insurance premiums |

| Score Creators | FICO, VantageScore | FICO, LexisNexis, TransUnion |

| Score Range | 300–850 (FICO) | 200–997 (varies by model) |

| Hard Inquiries Impact | Yes — can lower your score | No — insurance checks are soft pulls |

| Income Considered | No (but debt ratio matters) | No |

| Regulated By | CFPB, FCRA | State insurance commissioners |

| You Can Access It | Yes — free weekly at AnnualCreditReport.com | Sometimes — ask your insurer |

The biggest takeaway from that table? These are two separate tools, built by different people, for different purposes. Just because you’re great at one doesn’t mean you’re great at the other.

Why This Matters in Real Life (More Than You Think)

Let’s get into the real-life stuff — because this is where things get genuinely eye-opening.

Two People, Same Credit Score, Different Insurance Bills

Let’s say you and your friend both have a 700 credit score. You both drive the same type of car in the same city. You might expect to pay roughly the same auto insurance premium, right?

Not necessarily. If your credit history is more stable — older accounts, consistent payments, lower utilization — your insurance score might be meaningfully higher. The result? You could end up paying $200–$500 less per year than your friend for the exact same coverage.

That’s not a hypothetical. Research from the Consumer Federation of America has found that drivers with poor credit-based insurance scores can pay 50–100% more for auto insurance than those with excellent scores — even when all other risk factors are identical.

It Affects More Than Just Auto Insurance

Credit-based insurance scores are used for:

- Auto insurance (most common)

- Homeowners insurance

- Renters insurance

- Sometimes even life insurance (depending on state and insurer)

The impact on homeowners insurance can be just as significant. Insurers have found that people with lower insurance scores tend to file more home insurance claims — so they charge more to account for that expected risk.

You Could Have Good Credit and Still Be Overpaying

Here’s the part that really frustrates people when they find out: having a good credit score does not automatically mean you have a good insurance score.

Because the weighting is different, someone with a 750 credit score could have a below-average insurance score if their profile has characteristics that predict higher claims — like a high number of credit inquiries, recent account openings, or an unusually high revolving balance relative to their limits.

Meanwhile, someone with a 680 credit score but an extremely clean, stable credit history might have a great insurance score and be paying lower premiums.

Here’s where it gets frustrating: most people have never been told their insurance score even exists. They just see their premium go up at renewal and assume it’s their driving record or local crime rates — not this hidden score that’s quietly influencing the price they pay.

How Insurance Scores Actually Affect Your Premiums

Insurance companies use your score as part of a broader risk calculation. It doesn’t set your premium by itself — your driving history, the type of car you drive, where you live, and your age all play roles too. But the insurance score can be a surprisingly heavy factor.

The Premium Impact: What the Numbers Say

| Insurance Score Tier | Typical Auto Premium Impact | Typical Home Premium Impact |

|---|---|---|

| Excellent (900+) | Lowest rates — up to 40% savings vs. poor score | Up to 35% savings |

| Good (700–899) | Near-average rates — modest savings | Near-average rates |

| Fair (500–699) | Above-average rates — 20–40% more than excellent | Noticeably higher premiums |

| Poor (Below 500) | Highest rates — potentially double the ‘excellent’ rate | Significantly elevated premiums |

Think about what that means over the lifetime of your policy. If you’re paying $1,800/year for auto insurance but could qualify for $1,200 with a better insurance score — that’s $600 a year. Over five years, that’s $3,000 sitting on the table.

This is where people unknowingly lose hundreds — sometimes thousands — of dollars over time, all because of a score they didn’t know was being calculated.

Proven Strategies to Improve Both Scores (And Save Money)

Here’s the good news: because both scores draw from the same credit data, improving your credit habits helps both of them. It’s not always a 1-to-1 improvement, but the direction is the same.

Let’s walk through the most effective strategies — not the vague stuff you’ve heard before, but real, specific actions.

Step-by-Step: How to Check and Improve Your Insurance Risk Profile

This is the practical action plan. Follow these steps in order and you’ll have a clearer picture of where you stand — and a real path to improvement.

Go to AnnualCreditReport.com and pull all three credit reports (Equifax, Experian, TransUnion). They’re free, and you’re legally entitled to them.

Go through each report line by line and flag anything that looks wrong — unknown accounts, incorrect balances, outdated negative marks, or late payments you know were on time.

File disputes directly with the bureau(s) reporting the error. Submit online or via certified mail. The bureau has 30 days to investigate and respond.

Check your credit utilization across all cards. If you’re above 30% on any card or overall, make reducing that balance a priority — it’s the fastest-moving factor in your scores.

Set up autopay for the minimum payment on every account. Never let anything go 30+ days late again. This is the most important long-term habit you can build.

Ask your current insurer what scoring model they use and whether they can share information about your insurance score. Not all will tell you, but some will — and in a few states, they’re required to.

Get quotes from at least three competing insurers using a comparison platform. Even with the same score, different companies price risk differently. There’s real money to be found here.

Sign up for a credit monitoring service to track changes to your report in real time. This helps you catch errors quickly and see how your habits are moving your scores over time.

Repeat steps 1–3 every 12 months at minimum. Your situation changes, and so does the data on your reports.

Common Myths — Busted

There’s a lot of confusion around credit and insurance scores — and some of that confusion is genuinely costing people money. Let’s clear the air.

| Myth | Reality |

|---|---|

| “Insurance companies check your credit score” | They check a credit-BASED insurance score — a totally different calculation. |

| “Bad credit means no insurance coverage” | Most insurers are legally required to offer coverage, but your premiums may be higher. |

| “Checking your score hurts your insurance rates” | Insurance checks are soft inquiries. They don’t affect your credit score at all. |

| “Your insurance score never changes” | It updates regularly — sometimes monthly — based on your credit activity. |

| “All states allow insurance scoring” | California, Hawaii, Massachusetts, and Michigan ban or restrict its use for auto insurance. |

One more myth worth busting: the idea that you can’t do anything about your insurance score. You absolutely can — and the strategies in the previous section are exactly how. It just takes a little time and consistency.

Do You Even Have an Insurance Score? (It Depends on Where You Live)

Here’s something that surprises a lot of people: the rules around insurance scoring vary dramatically by state. In some states, insurers have almost complete freedom to use credit-based scores. In others, their hands are tied.

States That Restrict or Ban Insurance Scoring

If you live in one of the fully restricted states, your auto insurance premium is legally not allowed to be affected by your credit-based insurance score. Your driving record, vehicle type, location, and age carry the full weight instead.

If you live elsewhere, though? Your insurance score is almost certainly part of how your premium gets calculated — and you now know enough to do something about it.

Frequently Asked Questions

Final Thoughts: Two Scores, One Financial Life

At the end of the day, this isn’t just about numbers — it’s about how much money is quietly leaving your account every single month in the form of insurance premiums you could be paying less for.

Your credit score and your credit-based insurance score are not the same thing. They’re cousins, not twins. They share the same DNA (your credit data), but they were raised by different families with different goals. And ignoring the insurance score — which most people do, because they don’t even know it exists — is an expensive mistake.

The beautiful thing, though, is that the fixes overlap. Pay on time. Keep utilization low. Don’t open a bunch of new accounts at once. Monitor your reports. Dispute errors.

Do those things consistently, and both scores will move in the right direction. Your lenders will notice. Your insurer will notice — even if they never tell you.

And that money you save on premiums? That’s real money. Put it in your emergency fund, pay down debt, or invest it. Either way, it’s working for you instead of sitting in an insurer’s pocket.

You’ve got the full picture now. The next step is yours.

Quick Action Checklist

Pull your free credit reports at AnnualCreditReport.com today.

Set up autopay on every account — never miss a payment again.

Pay down credit card balances to get utilization under 30%.

Sign up for a credit monitoring tool to track changes in real time.

Get at least three new insurance quotes using a comparison platform — you might be surprised.

If you find errors on your report, dispute them in writing immediately.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Insurance pricing and credit scoring rules vary by state and insurer. Consult a licensed insurance agent or financial advisor for guidance specific to your situation.