Two drivers. Same car. Same age. Same zip code. Same spotless driving record. Yet one pays $900 more per year for car insurance.

The difference? Their credit scores.

Most Americans have no idea that the three-digit number that determines their mortgage rate or credit card APR also quietly shapes what they pay for auto and homeowners insurance. In fact, insurance companies run a version of a credit check on almost every applicant — and the results can swing premiums by hundreds of dollars annually.

In this guide you will learn:

- Why insurance companies check your credit in the first place

- How an insurance credit score differs from your regular FICO score

- Exactly how much poor credit can add to your premiums

- Which types of insurance are affected — and which ones are not

- The states that have banned or restricted the practice

- Seven practical steps to improve your credit and lower your insurance costs

- How to shop smarter for insurance quotes right now

Whether your credit is excellent, fair, or somewhere in between, understanding this connection can save you real money. Let’s dig in.

Check Your Insurance Rate in Under 2 Minutes

Your credit score may already be affecting how much you pay for insurance. Compare personalized quotes from top insurers to see exactly where you stand.

✔ Free quotes ✔ No obligation ✔ Takes under 2 minutes

📋 Table of Contents

- Why Insurance Companies Check Your Credit Score

- What Is an Insurance Credit Score?

- How Much Can Your Credit Score Change Your Premium?

- Which Types of Insurance Use Credit Scores?

- States Where Credit Scores Cannot Be Used

- Why Insurers Believe Credit Predicts Risk

- Real-Life Example: How Improving Credit Lowered Premiums

- Seven Steps to Improve Your Credit

- When Does a Better Credit Score Lower Your Insurance?

- How to Check Your Credit Score for Free

- How to Compare Insurance Quotes the Smart Way

- Common Myths About Credit Scores and Insurance

- Key Takeaways

- Frequently Asked Questions

1. Why Insurance Companies Check Your Credit Score

If you have ever applied for car insurance and wondered why the insurer asked for your Social Security number, this is the reason.

Insurance companies use a specialized version of credit data to predict how likely you are to file a claim. It sounds counterintuitive at first — what does paying a credit card bill on time have to do with whether you get into a fender bender? But insurers have decades of actuarial data suggesting there is a real statistical link.

According to the Federal Trade Commission (FTC), credit-based insurance scores are effective predictors of insurance losses under automobile policies.

The industry argument goes like this: people who manage their finances responsibly tend to be more careful in general — they drive more cautiously, maintain their homes better, and are less likely to submit unnecessary claims. Insurers call this the “credit-behavior correlation.”

Critics push back on this reasoning, arguing it can penalize lower-income Americans who carry more debt through no fault of their own. Several states have taken steps to limit or ban the practice (more on that in Section 5).

But in most of the country, credit-based insurance scoring is legal, widely used, and genuinely does affect what you pay. You can learn more about average insurance costs across the US to understand just how significant these differences can be.

💡 Industry Context

The use of credit-based insurance scores became widespread in the 1990s after studies by Fair Isaac Corporation (FICO) showed a statistical link between credit behavior and insurance claims.

2. What Is an Insurance Credit Score — and How Is It Different From Your FICO Score?

This is one of the most common points of confusion. Your regular credit score (the FICO Score most lenders use) and your insurance credit score are related but not identical. See our post on common credit score myths for more on this distinction.

Regular FICO Score vs. Insurance Credit Score

| Feature | Regular FICO Score | Insurance Credit Score |

|---|---|---|

| Purpose | Predict loan default | Predict insurance claims |

| Who uses it | Banks, lenders | Insurance companies |

| Score range | 300–850 | Varies by model |

| Hard inquiry? | Usually yes | Soft inquiry only |

The insurance credit score is a soft pull — it does NOT appear on your credit report and will NOT lower your regular credit score. You can shop for insurance quotes without any fear of hurting your FICO score.

What Factors Go Into an Insurance Credit Score?

| Factor | Approx. Weight | What It Means |

|---|---|---|

| Payment history | ~40% | Late or missed payments hurt the most |

| Outstanding debt / utilization | ~30% | High balances relative to limits are penalized |

| Length of credit history | ~15% | Older accounts signal stability |

| New credit accounts | ~10% | Many new accounts suggest financial stress |

| Credit mix | ~5% | Variety of credit types is a modest positive |

What insurance companies do NOT consider:

- Your income or employment status

- Your race, national origin, gender, or religion (prohibited by law)

- Your age (in most states)

- Disability or marital status

For reference, FICO’s insurance scoring methodology is publicly documented and widely used as the industry baseline.

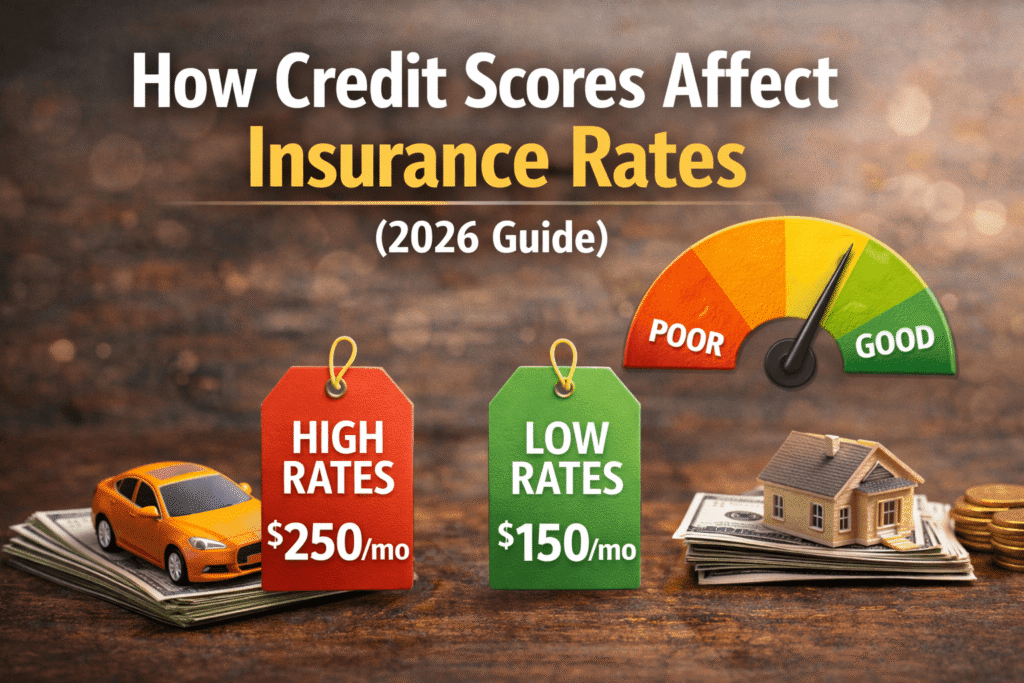

3. How Much Can Your Credit Score Change Your Insurance Premium?

Here is where things get eye-opening. The premium difference between excellent and poor credit can be staggering — and the numbers vary significantly by state and insurer.

Auto Insurance Rate Estimates by Credit Tier

The following figures represent national averages compiled from multiple insurer rate filings and consumer reports. Your actual rate will vary based on your state, vehicle, and coverage level.

| Credit Score Tier | Score Range | Avg Annual Premium | vs. Excellent |

|---|---|---|---|

| 🟢 Exceptional | 800–850 | $1,100 | Baseline |

| 🔵 Very Good | 740–799 | $1,250 | +14% |

| 🟡 Good | 670–739 | $1,500 | +36% |

| 🟠 Fair | 580–669 | $1,850 | +68% |

| 🔴 Poor | 300–579 | $2,300 | +109% |

Source: National Association of Insurance Commissioners (NAIC) rate data and consumer advocacy research.

Let that sink in: a driver with poor credit can pay more than double what an identical driver with exceptional credit pays — even with the same car, the same driving history, and the same coverage.

A Real-World Side-by-Side Comparison

Meet Marcus and David. They live two streets apart in Dallas, Texas. Both are 35 years old. Both drive a 2021 Honda Accord. Both have clean driving records. The only meaningful difference: Marcus has a 790 credit score and David has a 605.

| Marcus (790 Score) | David (605 Score) | |

|---|---|---|

| Annual Premium | $1,180 | $2,140 |

| Monthly Premium | $98 | $178 |

| Annual Difference | — | +$960 |

| 5-Year Difference | — | +$4,800 |

Over five years, David is essentially paying for a used car out of extra insurance costs — all because of a credit gap that has nothing to do with how he drives.

💡 Smart Money Tip

Many insurance companies penalize poor credit far more heavily than others. One insurer might charge David $960 more; another might only charge $300 more for the same coverage. Comparing quotes from multiple insurers is one of the fastest ways to reduce this penalty.

How Much Could You Save?

Drivers who compare insurance quotes often find savings of $400–$800 per year. Each insurer weighs credit differently — your current insurer may not be giving you the best deal.

✔ Free quotes ✔ No obligation ✔ Takes under 2 minutes

4. Which Types of Insurance Use Credit Scores?

Car insurance gets most of the attention, but it is not the only type of coverage affected by your credit profile.

🚗 Auto Insurance

This is by far the most common use of credit-based insurance scoring. The vast majority of major auto insurers — including GEICO, Progressive, Allstate, State Farm, and Nationwide — factor in credit scores when calculating premiums in states where it is permitted. See our guide to the cheapest car insurance companies to compare your options.

🏠 Homeowners Insurance

Homeowners insurance carriers also routinely use credit scores. A poor score can raise your annual homeowners premium by 20–50% compared to someone with excellent credit insuring the same home. When you consider that homeowners insurance can already run $1,500–$3,000+ per year depending on your state, this is a meaningful difference. The Insurance Information Institute (III) confirms that credit-based insurance scores are a standard underwriting tool for both auto and home policies in most states.

🏢 Renters Insurance

Yes, even renters insurance — which typically costs only $15–$30 per month — can be affected by credit scores. While the dollar impact is smaller, insurers in most states are permitted to use credit data to evaluate renters insurance applicants.

☂️ Umbrella Insurance

Umbrella policies (which provide liability coverage beyond your auto and home limits) may also involve credit review during underwriting, though the practice is less universal here than with auto and home.

❤️ Life Insurance — The Exception

Life insurance is the notable exception. Life insurers primarily rely on medical underwriting — your health history, age, lifestyle factors like smoking, and sometimes a medical exam. While some life insurance companies may do a soft credit pull as part of fraud screening, your credit score does not directly determine your life insurance premium.

🏥 Health Insurance — Also an Exception

Health insurance purchased through the Affordable Care Act (ACA) marketplace, employer-sponsored plans, or government programs like Medicaid and Medicare does not use credit scores for pricing. Your premiums are based on factors like age, location, plan tier, and tobacco use.

5. States Where Credit Scores Cannot Be Used for Insurance

Not every state allows insurers to use credit scores freely. Several states have passed legislation restricting or outright banning the practice — meaning if you live in one of these states, your credit score will not affect your insurance premium.

| State | Restriction Level | What It Means |

|---|---|---|

| California | Full Ban | Credit cannot be used for auto or home insurance |

| Hawaii | Full Ban (Auto) | Prohibited for auto insurance pricing |

| Massachusetts | Full Ban | Credit not used for auto or home pricing |

| Michigan | Restricted | Limited use only; reforms enacted 2019–2022 |

| Maryland | Restricted | Limits on using credit for renewals |

| All Other States | Permitted with Rules | Insurers may use credit scores with state oversight |

During the COVID-19 pandemic, several states — including California and New York — issued emergency orders temporarily prohibiting credit score use for insurance, recognizing that the pandemic’s economic disruptions unfairly affected consumers’ credit profiles. Some of those rules have since been extended or made permanent.

Always check your state’s Department of Insurance website for the most current rules in your area. A good resource is the NAIC State Insurance Regulation map.

6. Why Insurers Believe Credit Predicts Risk — and Why Critics Disagree

This debate has been going on for decades, and it is worth understanding both sides.

✅ The Insurance Industry’s Argument

Insurers point to actuarial research showing that people with lower credit scores statistically:

- File more insurance claims

- File larger claims on average

- Have higher rates of policy lapses and non-payment

From a pure risk-modeling standpoint, this correlation is real and measurable across large datasets.

❌ The Consumer Advocate’s Argument

Critics argue that credit-based insurance scoring:

- Disproportionately affects low-income Americans and communities of color

- Punishes people for economic hardships beyond their control

- Creates a compounding penalty

- Is not actually a measure of driving ability or home maintenance

The Consumer Federation of America has published extensive research on how credit scoring in insurance markets affects low-income policyholders. Where you land on this debate may depend on whether you prioritize actuarial precision or social equity. What is certain is that until more states ban the practice, most Americans need to manage this reality strategically. See also our article on common mistakes that make insurance more expensive.

7. Real-Life Example: How Improving Credit Lowered One Person’s Insurance Costs

Let’s make this concrete with a realistic scenario.

Sarah is 32 years old and lives in Austin, Texas. In early 2022, her credit score was 615 — a result of some missed payments during a difficult period after losing her job during the pandemic. Her annual auto insurance premium was $2,180.

Over the next two years, Sarah:

- Set up autopay for all her bills (eliminated late payments)

- Paid down her two credit cards from 78% utilization to 22%

- Disputed and corrected two errors on her credit report

- Kept her oldest credit card open even though she rarely used it

By early 2024, her credit score had climbed to 718. When her auto insurance renewal came up, she took the opportunity to shop around.

| 2022 (Score: 615) | 2024 (Score: 718) | |

|---|---|---|

| Annual Auto Premium | $2,180 | $1,340 |

| Monthly Cost | $182 | $112 |

| Annual Savings | — | $840 saved |

Sarah’s annual saving of $840 did not come from any dramatic life change — just consistent, strategic financial habits combined with actively shopping for a better quote. Her new insurer also happened to weigh credit less heavily than her old one, amplifying the savings. Sarah’s story is not unusual. It plays out for thousands of Americans every year who discover this credit-insurance connection and act on it.

Find Cheaper Insurance Quotes Today

You don’t have to wait to improve your credit to find savings. Some insurers weigh credit far less than others — comparing quotes can reveal a better deal right now.

Check Quotes From Top Insurers

✔ Free quotes ✔ No obligation ✔ Takes under 2 minutes

8. Seven Steps to Improve Your Credit and Lower Your Insurance Rates

Improving your credit is the most powerful long-term lever for lowering your insurance costs. These seven steps are proven and actionable — even if your credit is in rough shape right now.

Pay Every Bill on Time — Without Exception

Payment history is the single largest component of both your regular FICO score and your insurance credit score (approximately 40%). One 30-day late payment can drop your score by 50–100 points. The fix is simple but requires discipline: set up automatic payments for every recurring bill. Read more about how late payments affect your credit score.

Reduce Your Credit Card Balances

Credit utilization — how much of your available credit you are using — is the second-biggest factor. Try to keep utilization below 30% on each card and below 10% across all cards if possible. Paying down a card from 80% utilization to 25% can raise your score meaningfully within 30–60 days. See our guide on how to avoid credit card debt for practical strategies.

Check Your Credit Reports for Errors

This is one of the most overlooked steps, yet the Consumer Financial Protection Bureau (CFPB) estimates that a significant portion of consumer credit reports contain errors. You are entitled to a free annual credit report from all three bureaus — Equifax, Experian, and TransUnion — at AnnualCreditReport.com. Our guide on removing negative items from your credit report walks you through the dispute process step by step.

Avoid Opening Too Many New Accounts at Once

Each time you apply for new credit, a hard inquiry is recorded. Multiple new accounts in a short period can signal financial stress to insurers and scoring models. Unless you need new credit urgently, space out applications and avoid opening accounts just to increase your total limit.

Keep Your Oldest Credit Accounts Open

The length of your credit history matters. Closing an old account — even one you no longer use — can shorten your average account age and potentially hurt your score. Keep old cards active by making a small purchase on them occasionally and paying it off immediately.

Diversify Your Credit Mix

Having a variety of credit types — credit cards, installment loans, a mortgage — is modestly positive for your score. This does not mean you should take out unnecessary loans, but if you only have credit cards and you are considering financing a purchase anyway, doing so through a traditional installment loan can have a small positive effect over time.

Re-Shop Your Insurance Every Year

Even before your credit score improves significantly, shopping for quotes annually gives you two advantages: (1) you may find an insurer that penalizes your current credit tier less heavily, and (2) as your score improves, you will be able to see the premium reductions materialize in real time. Set a reminder to compare quotes at every policy renewal. Learn how insurance quotes are calculated to know exactly what you’re comparing.

💡 Timeline Tip

Most people who follow steps 1–3 consistently see measurable credit score improvements within 6–12 months. Major improvements — enough to move from one credit tier to the next — typically take 12–24 months of consistent habits.

9. When Does a Better Credit Score Actually Lower Your Insurance?

Improving your credit score does not automatically trigger an immediate insurance rate reduction. Here is how it actually works in practice.

📅 At Policy Renewal

Most insurers re-evaluate your credit score at each renewal period (typically every 6 or 12 months). If your score has improved, you should see the benefit reflected in your new premium. However, if you stay with the same insurer without shopping around, you may not see the full benefit — insurers do not always proactively offer you the best possible rate.

🔄 When You Switch Insurers

Shopping for a new policy with a different insurer is often the fastest way to benefit from a higher credit score. New insurers will pull your insurance credit score fresh, meaning improvements you have made will be fully reflected in the quote they offer.

⚡ After a Significant Life Event

Certain life events — paying off a large debt, resolving a collections account, or correcting a credit report error — can cause a meaningful score jump relatively quickly. If you experience one of these events, it may be worth reaching out to your insurer or shopping for new quotes even mid-policy.

10. How to Check Your Credit Score for Free

You have multiple options for monitoring your credit score at no cost. Here are the most reliable ones:

| Resource | What You Get | Cost |

|---|---|---|

| AnnualCreditReport.com | Full credit report from all 3 bureaus | Free (federally mandated) |

| Credit card issuer portals | Monthly FICO or VantageScore updates | Free for cardholders |

| Experian.com | Experian credit score + report | Free (basic tier) |

| Credit Karma | TransUnion and Equifax VantageScores | Free (ad-supported) |

| CFPB Resource Page | Tools and dispute guidance | Free |

Important: Checking your own credit score is a soft inquiry and does NOT affect your credit score in any way. You can check as often as you like without any impact.

Helpful resource: CFPB’s guide to understanding your credit report is an excellent starting point for anyone new to credit monitoring. Also check our article on what the average credit score in the US looks like to see where you stand nationally.

11. How to Compare Insurance Quotes the Smart Way

Understanding the credit-insurance connection is valuable, but taking action by comparing quotes is where the savings actually happen.

Here is the key insight that most people miss: insurance companies weigh credit scores differently. One insurer’s algorithm might penalize a 640 score by $600 per year; another’s might penalize the same score by only $150. That means the same driver with the same credit score can receive dramatically different quotes from different insurers.

What to Look for When Comparing Quotes

- Compare identical coverage levels — same liability limits, same deductibles, same uninsured motorist coverage

- Get at least 3–5 quotes, not just 1 or 2

- Look at the full annual cost, not just the monthly payment

- Check the insurer’s financial strength rating (A.M. Best or Moody’s)

- Read reviews focused on claims handling, not just price

When to Shop

The best times to shop for insurance quotes are:

- 30–45 days before your current policy renews

- After any significant credit score improvement

- After a major life event (move, new car, marriage, divorce)

- Once per year as a general practice

Compare Quotes From Top Insurance Companies

Insurance companies calculate credit risk differently. The same driver can receive very different quotes from different insurers. Comparing multiple offers takes just a few minutes and can reveal significant savings.

✔ Free quotes ✔ No obligation ✔ Takes under 2 minutes

12. Common Myths About Credit Scores and Insurance

There is a lot of misinformation floating around this topic. Let’s clear up the most common misconceptions.

| Myth ❌ | Reality ✅ |

|---|---|

| Checking your credit before buying insurance will hurt your score | Shopping for insurance uses a soft inquiry — it never appears on your credit report and has zero impact on your score |

| Credit scores only affect loans and credit cards | Credit scores are used in auto insurance, homeowners insurance, renters insurance, and umbrella policies across most of the US |

| All insurance companies use credit the same way | Every insurer has a proprietary model. Credit carries very different weight at different companies — which is exactly why shopping around pays off |

| Income affects your insurance credit score | Income is not used in insurance credit scoring. Payment history, utilization, and account age are the key factors |

| Once you have poor credit, your insurance rate is stuck | Rates are re-evaluated at renewal. Improving your credit over time directly translates to lower premiums — and switching insurers accelerates the benefit |

| A bankruptcy permanently ruins your insurance rates | Bankruptcy does hurt insurance scores significantly, but the impact diminishes over time (typically 5–7 years as it ages on your report) |

13. Key Takeaways

Summary: What You Need to Remember

-

✓

Your credit score is one of the most significant factors in calculating your auto and homeowners insurance premium in most U.S. states. -

✓

The gap between excellent and poor credit can mean $1,000+ more per year in insurance costs — for identical coverage. -

✓

Insurance companies use a specialized insurance credit score, not your standard FICO score. The check is a soft pull and does not affect your credit. -

✓

California, Hawaii, and Massachusetts currently prohibit credit-based insurance scoring for auto coverage. Other states have varying restrictions. -

✓

Paying bills on time and reducing credit card utilization are the fastest ways to improve your insurance credit score. -

✓

Different insurers weigh credit very differently — comparing 3–5 quotes every year is one of the single most effective ways to lower your insurance costs. -

✓

Credit score improvements are reflected in insurance premiums at renewal or when you switch to a new insurer.

14. Frequently Asked Questions

Find the Best Insurance Rate for Your Credit Score

Your credit score can significantly affect your insurance premium — often by hundreds of dollars a year. The most effective way to offset this is to compare quotes from multiple insurers, since each company evaluates credit differently.

✔ Free quotes ✔ No obligation ✔ Takes under 2 minutes

15. Final Thoughts

Credit scores influence far more than most people realize. Beyond loans and credit cards, they quietly shape what you pay for car insurance, homeowners insurance, renters insurance, and more — in most states, every single year.

The frustrating reality is that this can feel like a double penalty: financial hardship hurts your credit, and poor credit makes insurance more expensive, making it harder to recover financially. That cycle is real.

But the good news is also real: the same habits that improve your credit — on-time payments, lower balances, clean credit report — directly translate into lower insurance premiums over time. And in the short term, simply comparing quotes across multiple insurers can cut your costs immediately, regardless of where your credit stands today.

You do not have to accept the first rate you are quoted. You do not have to stay with your current insurer out of inertia. And you do not have to wait for your credit to be perfect before you start saving.

Start with what you can control today.